Table of Contents >> Show >> Hide

- Cloud 100, Explained: Why This Cohort Matters

- Why Growth Fell: 6 Forces That Turned 100% Into 55%

- 1) The “SaaSacre” hangover and multiple compression

- 2) Customer budget tightening (and the rise of CFO-led procurement)

- 3) Cloud spend optimization hit vendors’ top lines

- 4) Sales cycles lengthened and pipeline converted more slowly

- 5) The post-pandemic pull-forward effect faded

- 6) Intentional self-slowdown: choosing efficiency over speed

- How They Became More Profitable: The Efficiency Flywheel

- The New Metrics That Quietly Took Over the Cloud Economy

- The Profitable Growth Playbook: What Cloud 100 Companies Actually Did

- 1) Protect gross margin like it’s the roof over your runway

- 2) Make sales and marketing earn its keep (channel-by-channel)

- 3) Pricing and packaging became a profitability lever, not a last resort

- 4) Right-size the org without gutting innovation

- 5) Shift from “growth at all costs” to “growth at optimal cost”

- “Slower Growth” Doesn’t Mean “Smaller Opportunity”

- What This Means If You’re Building, Buying, or Betting on Cloud

- Conclusion

- Field Notes: of Real-World “Efficiency Era” Experiences

Remember when “growth at all costs” wasn’t a cautionary taleso much as a corporate love language? If you were a top-tier

private cloud company in 2021–2022, you could grow 100% year over year, raise at eye-watering multiples, and still have enough

budget left over to sponsor a conference featuring a DJ who “used to open for someone famous.”

Then 2023 happened. Suddenly, the Cloud 100Forbes’ annual list of the world’s top private cloud companies, built with Bessemer

Venture Partners and Salesforce Ventureslooked less like a fireworks show and more like a controlled burn (pun absolutely intended).

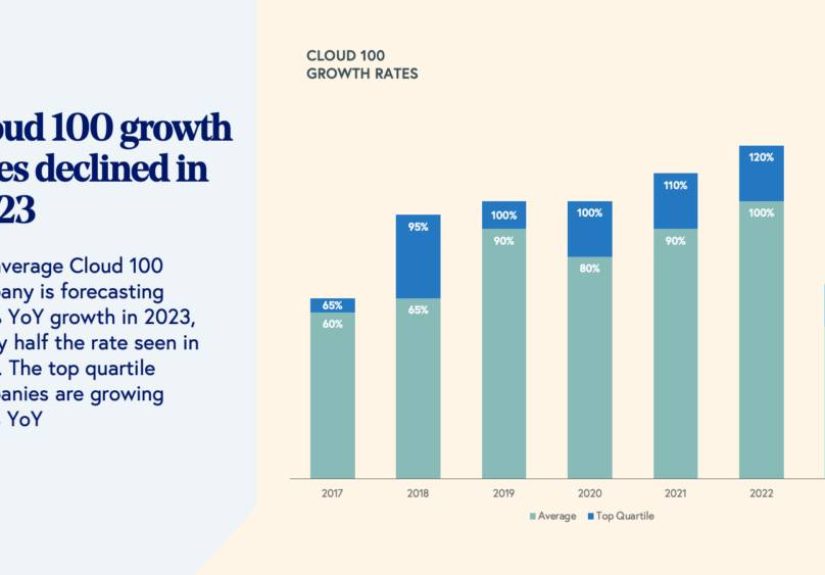

The headline stat says it all: average revenue growth for the Cloud 100 dropped from around 100% in 2022 to about 55% in 2023. And yet,

profitability and cash-flow discipline improved sharply. In other words: slower sprint, stronger lungs.

This isn’t a story about “the cloud is doomed.” It’s a story about the cloud growing upswapping caffeine-fueled hypergrowth for a more

sustainable (and frankly more IPO-friendly) operating model. Let’s unpack why Cloud 100 growth slowed so dramatically, how these companies

became meaningfully more profitable, and what the new playbook for profitable growth looks like in the efficiency era.

Cloud 100, Explained: Why This Cohort Matters

The Cloud 100 is often treated like the honor roll of private cloud computing: companies that are big, influential, and typically category-defining.

But it’s also a benchmark set. When a cohort this strong sees its growth rate fall nearly in half, it’s not a quirky data pointit’s a signal that the

market has changed for everyone.

Bessemer’s Cloud 100 benchmarks show the pivot clearly. The same group that posted roughly 100% average growth in 2022 saw average growth fall to 55% in 2023,

with top-quartile companies still growing faster (around 70%)but not at the “strap-a-rocket-to-it” levels of the prior cycle. At the same time, the cohort’s

focus shifted hard toward efficiency: nearly a quarter of Cloud 100 companies were already cash-flow positive, and a large majority had line-of-sight to breakeven

or profitability over the next 12–24 months.

The backdrop matters too. The Cloud 100’s aggregate value contracted year over year in 2023after years of expansion. Yet the cohort remained enormous,

reaching roughly the mid-$600B range in total equity value. Translation: these are still giants. They just stopped pretending gravity was optional.

Why Growth Fell: 6 Forces That Turned 100% Into 55%

1) The “SaaSacre” hangover and multiple compression

Public cloud software valuations fell sharply in 2022, which re-priced private markets whether founders liked it or not. When public comps compress, private investors

stop paying “future greatness” prices for “present vibes.” That shift pushed boards and leadership teams to prioritize durable unit economics and cash generation.

2) Customer budget tightening (and the rise of CFO-led procurement)

In 2023, many enterprises and mid-market buyers scrutinized software spend more aggressively. Deals took longer. Committees got bigger. Renewals got negotiated harder.

If your product was “nice to have,” you had a harder time expanding. If you were “must have,” you still had to prove it with measurable ROI.

3) Cloud spend optimization hit vendors’ top lines

Customers didn’t just slow new purchases; they optimized existing usage. That matters a lot in modern SaaSespecially for usage-based pricing and infrastructure-linked

revenue. When customers right-size consumption, vendors feel it like a cold breeze through the ARR forecast.

4) Sales cycles lengthened and pipeline converted more slowly

Even elite cloud companies reported longer sales cycles and tighter budgets across the market. That pushes revenue to the rightsometimes by a quarter, sometimes by

a yearreducing near-term growth rates even if long-term demand remains intact.

5) The post-pandemic pull-forward effect faded

A slice of 2020–2021 growth was a pull-forward: urgent digitization, remote work adoption, and fast cloud migration. By 2023, the “we need this yesterday” buying

behavior cooled. Mature categories started behaving like, well, mature categories.

6) Intentional self-slowdown: choosing efficiency over speed

This is the part founders don’t always say on earnings calls: sometimes you slow growth on purpose. When you cut unproductive spend, reduce discounting, tighten

qualification, or stop chasing low-quality expansion, revenue growth can dipwhile margins and cash flow improve dramatically. In 2023, “optimal growth” became the

new flex.

How They Became More Profitable: The Efficiency Flywheel

Here’s the central paradox of the Cloud 100 in 2023: growth slowed, but business quality improved. Many companies didn’t get weakerthey got sharper.

That’s because profitability in cloud isn’t only about “cut costs.” It’s about finding the spend that actually compounds.

Cloud businesses often have strong structural advantagesrecurring revenue, low marginal distribution costs, and retention dynamics that can be very resilient.

When teams apply discipline to that model, the results can be powerful: higher free cash flow, longer runway, and the ability to raise capital (or IPO) from a position

of strength rather than necessity.

Importantly, markets started rewarding this pivot more directly. The valuation conversation became less about “How fast are you growing?” and more about “How efficiently

do you grow, and can you produce real cash?” That’s where metrics like free cash flow margin, burn multiple, and Rule of 40-style frameworks moved from nerdy spreadsheets

into the boardroom spotlight.

The New Metrics That Quietly Took Over the Cloud Economy

Burn multiple (capital efficiency without the fluff)

Burn multiple is a simple idea with sharp teeth: how much net burn does it take to generate a dollar of net new ARR? Lower is better.

It forces a conversation about efficiency, not just speed. If you’re burning heavily for modest new ARR, the metric makes it painfully obvious.

Rule of 40 (and its modern cousins)

The classic “Rule of 40” combines growth and profitability into one benchmark (definitions varysome use EBITDA margin, others use free cash flow margin).

In the efficiency era, leadership teams used it less as a trophy and more as a steering wheel: if growth slows, margins must improve to keep the company attractive.

Net revenue retention and expansion quality

When new customer acquisition becomes harder, the fastest path to healthier growth is often better retention and smarter expansion.

Cloud 100 leaders leaned into customer success, product-led adoption, and pricing/packaging strategies that improve expansion without relying on endless discounting.

The Profitable Growth Playbook: What Cloud 100 Companies Actually Did

“Be more efficient” is not a plan. It’s a fortune cookie. The plan lives in specific leversespecially the ones that improve profitability without crushing long-term

product advantage. Here are the biggest moves that defined Cloud 100 efficiency in 2023.

1) Protect gross margin like it’s the roof over your runway

Gross margin is the ceiling for long-term profitability. Many cloud leaders focused on infrastructure efficiency: optimizing compute, storage, and networking costs;

improving code performance; renegotiating vendor contracts; and tightening internal usage. Even modest improvements at scale can turn into meaningful free cash flow.

2) Make sales and marketing earn its keep (channel-by-channel)

Instead of “spend more to grow,” teams got specific: which channels produce the best CAC payback? Which segments retain and expand better?

Which sales motions close faster? The result was a reallocation of spend toward what worksless “spray and pray,” more “aim and confirm.”

3) Pricing and packaging became a profitability lever, not a last resort

In a tighter budget environment, pricing discipline matters. Cloud 100 leaders refined packaging, added ROI-aligned tiers, improved monetization of premium features,

and reduced overly generous discounts that boosted bookings but harmed long-term revenue quality.

4) Right-size the org without gutting innovation

Many companies cut roles and restructured teams to match the new realitypainful, but often necessary. The best operators tried to cut “complexity tax” and duplicate work,

not core product capability. The goal: keep building, but with fewer internal handoffs and more measurable output.

5) Shift from “growth at all costs” to “growth at optimal cost”

This is where Cloud 100 companies separated themselves from the pack: they didn’t abandon growth; they demanded a better return on growth.

That meant tighter forecasting, better pipeline quality, and operating discipline that made growth more sustainable.

“Slower Growth” Doesn’t Mean “Smaller Opportunity”

The cloud market didn’t shrink; it matured. In fact, Cloud 100 companies continued reaching major milestones while staying private longer.

A striking benchmark: roughly 95% of the Cloud 100 cohort was expected to surpass $100M in ARR (the “Centaur” milestone) by the end of 2023.

That kind of scale is not a recession hobby.

And the story didn’t end with 2023’s slowdown. Benchmarks in the following years showed growth re-accelerating for many leadershelped by AI-driven product expansion

and new categories. The cloud model didn’t break; it rebalanced.

What This Means If You’re Building, Buying, or Betting on Cloud

If you’re a founder or operator

Your growth rate is a score, not a strategy. The strategy is: durable retention, efficient acquisition, strong gross margins, and a product roadmap that actually earns

expansion. The new gold standard is profitable growthbecause it keeps options open (raise, IPO, M&A, or just keep printing cash).

If you’re an investor

The efficiency era makes quality easier to spot. Metrics like burn multiple, net retention, and margin trajectory tell you whether growth is “healthy” or “borrowed.”

In a world where capital isn’t free, the best companies still winjust with fewer fireworks and more fundamentals.

If you’re a customer

You may notice vendors getting sharper: clearer pricing, stronger ROI narratives, more focus on retention and customer experience. The best cloud companies will keep

innovatingespecially with AIwhile proving they can do it without constantly raising more money.

Conclusion

The Cloud 100’s 2023 story is a pivot, not a collapse. Yes, average growth slowed dramaticallyfrom around 100% in 2022 to about 55% in 2023. But that slowdown came

with a meaningful upgrade in business quality: more cash-flow discipline, lower burn, and a stronger focus on operating leverage. In many ways, this is what success

looks like when the market stops rewarding speed alone and starts rewarding control.

The punchline (because every cloud story deserves one): Cloud 100 companies didn’t stop being ambitious. They just stopped funding ambition with wishful thinking.

And in a market that cares about profitable growth, that’s not a concessionit’s an advantage.

Field Notes: of Real-World “Efficiency Era” Experiences

If you want to understand the Cloud 100 shift in 2023, don’t start with chartsstart with calendars. The “experience” of the slowdown looked like recurring meetings

that didn’t exist in 2021: weekly cash reviews, pipeline reality checks, cloud spend audits, and pricing committees that suddenly had teeth. Teams that used to plan

quarters around “how fast can we hire?” started planning around “what’s the smallest team that can ship the roadmap without breaking production?”

Sales leaders felt it first. Deals that used to close with a champion and a handshake became multi-stakeholder projects: security review, procurement negotiation,

CFO sign-off, and the dreaded “we’re evaluating three vendors” email. The healthiest teams didn’t panicthey tightened qualification, pushed for clear ROI, and learned

to love smaller landings that expanded over time. The vibe changed from “win at all costs” to “win the right deals and keep them.”

Product teams experienced a different kind of pressure: fewer “moonshots for fun,” more “ship what improves retention.” The most valuable features became the ones that

saved customers money, reduced manual work, or made compliance easier. Adoption and time-to-value became everyone’s business, not just customer success. A surprising

number of roadmaps got simplerand betterbecause teams stopped building for hypothetical buyers and started building for the users already paying.

Finance and ops teams became the unexpected protagonists. Burn multiple wasn’t just a metric; it was a narrative device. It helped answer uncomfortable questions like:

“Is this spend buying real growth or just motion?” Budgets shifted toward high-conviction channels and away from activities that looked good in slide decks but didn’t

translate into retained revenue. Forecasts got more conservative, then more accurate. Nobody bragged about “efficiency” in 2021; in 2023, it became a badge of honor.

Culture changed too. In the growth-at-all-costs era, companies often celebrated scale for its own sakeheadcount, offices, events, and “we’re hiring in 12 countries”

announcements. In the efficiency era, celebration looked more like: “We improved gross margin,” “our net retention stabilized,” “our CAC payback dropped,” or

“we hit cash-flow breakeven.” Not as flashy, but a lot more durable.

And then there’s the emotional experience: the moment teams realized profitability wasn’t an enemy of innovationit was a form of freedom. When a company can fund its

roadmap with its own cash flow (or at least burn less while growing), it gets to choose its timing. It can raise because it wants to, not because it has to. It can

negotiate from strength. It can survive a longer IPO winter. That’s the quiet superpower behind the Cloud 100’s 2023 shift: slower growth, yesbut a sturdier machine

underneath it, built to last longer than the hype cycle.