Table of Contents >> Show >> Hide

- What “Moneycrashers and Bluevine” Really Means

- Why Money Crashers Matters in This Conversation

- What Bluevine Actually Brings to the Table

- Why Review Sites Keep Talking About Bluevine

- Where Bluevine Looks Strongest

- Where the Hype Needs a Seatbelt

- So, Is Bluevine a Good Match for the Money Crashers Audience?

- The Bigger Lesson Behind Moneycrashers and Bluevine

- Experience Section: What This Looks Like in Real Life

- Final Thoughts

Generated with GPT-5.4 Thinking

Put “Money Crashers” and “Bluevine” in the same sentence, and you get a surprisingly useful snapshot of modern small-business finance. One is a personal finance publisher built around plain-English money advice. The other is a digital business banking platform built for owners who would rather run payroll, send invoices, and chase growth than sit in a bank lobby under fluorescent lights that look like they were last updated during the fax machine era.

Together, they tell a bigger story about what today’s entrepreneurs want from financial tools: fewer fees, less friction, more yield on idle cash, and a platform that understands that “small business owner” often means “accountant, salesperson, operations manager, and emergency IT department, all before lunch.” If you’re trying to understand why Bluevine keeps showing up in business banking conversations and why a site like Money Crashers would pay attention to it, this is the article for you.

What “Moneycrashers and Bluevine” Really Means

On the surface, the phrase sounds like the title of an odd buddy comedy. In practice, it points to the intersection of financial education and financial products. Money Crashers represents the content side: reviews, explainers, comparisons, and consumer-focused analysis. Bluevine represents the product side: a fintech-driven banking and lending option for freelancers, startups, and growing small businesses.

That combination matters because business owners do not choose financial tools in a vacuum. They compare. They search. They read reviews while drinking coffee that has gone cold because they were also answering client emails. And when they do, they tend to gravitate toward publishers that explain things without sounding like a legal disclaimer wearing a necktie.

In that sense, Money Crashers and Bluevine belong in the same conversation. One helps readers ask smarter questions. The other tries to be a modern answer to those questions.

Why Money Crashers Matters in This Conversation

Money Crashers has built its brand around making financial literacy less intimidating and more practical. Its editorial voice is meant to be actionable, useful, and readable for normal humans, not just spreadsheet enthusiasts and people who say things like “asset allocation” at barbecues. The site covers spending, saving, investing, borrowing, and increasingly, small-business money management.

That matters because a lot of business owners are not looking for abstract theories. They want answers to very real questions: Which account charges fewer fees? Which platform helps separate business and personal money? Which option makes cash flow less chaotic? Which tool works for a freelancer today and still makes sense if that freelancer turns into a five-person agency next year?

Money Crashers fits into this space as a translator. It takes the messy world of financial products and turns it into something readers can evaluate. It is not a bank, and it is not a licensed adviser. It is an information layer. That makes it especially relevant when discussing products like Bluevine, which can sound amazing in a headline but still deserve a closer look.

What Bluevine Actually Brings to the Table

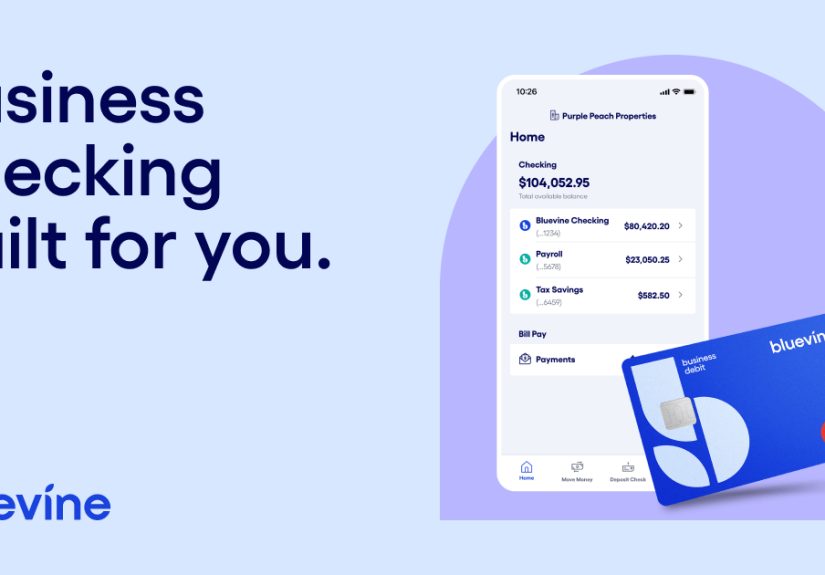

Bluevine has become one of the most talked-about names in online business banking because its core offer is easy to understand. The platform centers on a business checking experience with no monthly fees on its Standard plan, no minimum balance requirement, unlimited transactions, and free standard ACH transfers. For a lot of small-business owners, that alone is enough to get attention. Traditional business banking has a talent for making simple checking feel weirdly expensive.

Bluevine also leans hard into what many reviews highlight as its headline feature: the chance to earn interest on checking balances. Eligible customers on the Standard plan can earn 1.3% APY when monthly activity requirements are met, while upgraded plans can offer up to 3.0% APY. That may not sound thrilling until you remember how many business checking accounts historically paid somewhere between “almost nothing” and “technically this number exists.”

The platform’s appeal goes beyond yield. Bluevine has pushed into a broader set of business finance tools, including invoicing, payment links, Tap to Pay, bill pay, accounts payable support, and sub-accounts for budgeting. In plain English, that means it is trying to become less of a digital filing cabinet for your money and more of an operating system for your business cash flow.

Business Checking That Feels Built for 2026

Bluevine’s checking product is clearly designed for digital-first businesses. If you invoice clients, accept payments online, pay contractors electronically, and want visibility across multiple cash buckets, the platform makes intuitive sense. It also offers access to no-fee MoneyPass ATMs and expanded FDIC protection up to $3 million per depositor through Coastal Community Bank and program banks.

That combination of low fees, high APY, and automation-friendly tools explains why Bluevine keeps landing on best-of lists. Publishers evaluating business checking accounts tend to reward the same themes over and over: low maintenance costs, digital usability, solid yields, and features that help owners move faster. Bluevine checks a lot of those boxes with a very loud marker.

Lending and Cash-Flow Support

Bluevine is not just about checking. It also offers a business line of credit of up to $250,000 and partner term-loan options up to $500,000. Published eligibility guidance for the line of credit includes being in business for at least 12 months, annual revenue of at least $120,000, and a personal FICO score of 625 or higher, with some applicants seeing funding decisions quickly.

That matters because small businesses rarely experience cash flow in a neat, cinematic montage. It is lumpy. Clients pay late. Inventory shows up early. Tax season appears like a jump scare. A platform that combines checking with access to working capital has a natural advantage in marketing because it speaks directly to the stress points owners actually feel.

Why Review Sites Keep Talking About Bluevine

When you scan the broader personal finance and small-business media landscape, a pattern emerges. Bluevine is often praised for being a strong fit for freelancers, solopreneurs, online businesses, and cash-light companies. Reviewers tend to like the fee structure, the interest-earning potential, and the expanding suite of built-in business tools.

Money Crashers fits right into that pattern. Its editorial framework emphasizes practical value: low fees, easy-to-understand features, room to grow, and usefulness for real-world business owners. That is exactly the kind of environment where Bluevine tends to perform well. It is not trying to win on branch access or old-school prestige. It is trying to win on efficiency.

And to be fair, efficiency is having a moment. Business owners increasingly expect banking to work like the rest of their software stack: fast to open, simple to navigate, integrated with the tools they already use, and unlikely to surprise them with a “service fee” that feels like it was invented by someone who hates joy.

Where Bluevine Looks Strongest

The strongest case for Bluevine is pretty straightforward. It is a smart fit for business owners who want an interest-bearing business checking account, mostly operate online, and value built-in payment and budgeting tools. It is especially appealing for freelancers, agencies, consultants, e-commerce sellers, and service businesses that do not deal with piles of cash every week.

Bluevine also stands out because it reflects how small businesses increasingly manage money: digitally, remotely, and with multiple moving parts. A single dashboard that can support checking, sub-accounts, invoices, payment acceptance, and financing feels more relevant today than a bank relationship based mostly on proximity to a branch and a bowl of mystery peppermints.

Where the Hype Needs a Seatbelt

That said, Bluevine is not a universal answer. If your business handles frequent cash deposits, the experience gets less charming. Reviewers consistently flag cash deposits as a weakness because they come with fees and limits. If your company collects a lot of physical cash, a traditional bank or credit union may still be the more practical choice.

There is also the classic fintech reality check: Bluevine is a financial technology company, not a bank. That does not make it unsafe, but it does mean users should understand the structure. Banking services are provided through partner institutions, and the extra FDIC coverage works through that partner-bank model. For many owners, that is perfectly fine. For others, it is one more detail to read before clicking “open account.”

Finally, the best parts of Bluevine tend to matter most when your business already works digitally. If you still write lots of checks by hand, rely on in-person branch help, or need highly specialized treasury services from day one, Bluevine may feel a little too sleek for your messier, more analog reality.

So, Is Bluevine a Good Match for the Money Crashers Audience?

In many cases, yes. The overlap is strong. Money Crashers readers are usually looking for ways to reduce waste, simplify money management, and choose products that offer visible value. Bluevine speaks directly to those priorities. It cuts out common fee pain points, adds yield where many competitors do not, and packages practical business tools in one place.

But the smarter takeaway is not “Bluevine is perfect.” It is that Bluevine fits a specific kind of user especially well: the digitally comfortable business owner who wants modern banking, easy cash-flow management, and optional access to working capital without dealing with the slower rhythms of traditional business banks.

The Bigger Lesson Behind Moneycrashers and Bluevine

The real value of this topic is not just the product itself. It is what the pairing reveals about modern money content. A site like Money Crashers succeeds when it helps readers separate marketing from usefulness. A platform like Bluevine succeeds when the actual product holds up after that scrutiny.

That is why this pairing works so well as a topic. It is not just a brand and a review site. It is a case study in how people make financial decisions now. They do research first, compare features second, and give loyalty last. The days of choosing a business bank because your uncle liked the branch manager are fading fast.

Experience Section: What This Looks Like in Real Life

The experience of moving from reading about Bluevine on a site like Money Crashers to actually evaluating it for your business is often less dramatic than people expect, but more revealing. At first, the appeal is emotional as much as practical. You read about no monthly fees, interest on checking, and built-in payment tools, and your brain does a tiny victory lap. Finally, a business account that does not seem designed to punish ambition. That first impression matters because many small-business owners already feel overcharged and under-served by legacy banks.

For a freelancer, the experience usually starts with organization. Imagine a copywriter, designer, or developer who has spent two years mixing business income with personal expenses in one overworked checking account. After reading an explainer or review, they realize the issue is not only bookkeeping; it is mental clutter. A separate business account creates a cleaner boundary. Bluevine becomes appealing not because it is flashy, but because it promises a more adult financial setup without the usual administrative headache. The result is often less stress at tax time and a more accurate sense of what the business is actually earning.

For a small agency or consulting firm, the experience shifts toward cash-flow visibility. This kind of owner is not just asking, “Where is my money?” They are asking, “Which money is reserved for payroll, which part is for taxes, and how much is actually safe to spend?” That is where features like sub-accounts, digital transfers, invoicing, and payment acceptance start to feel less like bonus features and more like oxygen. When a product helps owners label and separate funds by purpose, they stop making decisions based on one scary-looking account balance and start making decisions with context.

For an e-commerce seller or online service business, the experience often comes down to speed. These owners usually care less about marble floors and more about workflow. Can they send invoices quickly? Can they accept payments without adding another three apps to the stack? Can they keep money moving without paying a fee every time the account blinks? In that environment, Bluevine feels attractive because it treats banking as an operational tool instead of a ceremonial event. It supports the rhythm of online business, which is usually fast, messy, and allergic to unnecessary steps.

Of course, not every experience is glowing. A cash-heavy business may read the same review and realize Bluevine is not the best fit after all. A restaurant owner, market vendor, or repair shop that deals with frequent cash deposits can quickly run into the fine print that digital-first businesses barely notice. That experience is important too, because it shows the value of financial review content done properly. The best outcome is not always “yes.” Sometimes the smartest result of reading about Money Crashers and Bluevine is discovering that Bluevine is great for someone else and only decent for you.

There is also a quieter emotional experience tied to products like Bluevine: relief. Not excitement. Not brand loyalty. Relief. Relief that the account is understandable. Relief that fees are not hiding behind every menu. Relief that a banking tool finally acknowledges how small businesses actually operate in 2026. That feeling is why Bluevine keeps showing up in reviews and comparisons. It is not because the company discovered magic. It is because it solved several very ordinary frustrations at once.

And that is probably the most honest experience-based takeaway of all. Money Crashers-style readers are not looking for a banking soulmate. They are looking for a better deal, cleaner systems, and fewer financial migraines. Bluevine earns attention because, for the right kind of business owner, it delivers exactly that. Not perfection. Just meaningful improvement. In business banking, that is sometimes more impressive than perfection anyway.

Final Thoughts

“Moneycrashers and Bluevine” is really a story about smarter business banking through smarter research. Money Crashers represents the practical editorial lens that helps readers question fees, evaluate features, and think beyond marketing copy. Bluevine represents the kind of modern financial platform that has benefited from that shift in expectations. For online-first entrepreneurs, freelancers, and growing small businesses, Bluevine can be a compelling choice. For cash-heavy or branch-dependent businesses, maybe not so much.

The smart move is not to assume Bluevine is the best account for everyone. The smart move is to use the same logic that made the topic interesting in the first place: compare honestly, read carefully, and pick the business checking account that makes your money easier to manage, not harder to explain.