Table of Contents >> Show >> Hide

- What Is a Stock Market Bubble?

- Why the Stock Market Is Booming

- The Bubble Warning Signs Investors Are Watching

- The Case That This Is Not a Bubble

- How Today Compares With Past Market Bubbles

- What Could Pop the Bubble If There Is One?

- What Investors Should Watch Instead of Guessing

- So, Could the Stock Market Boom Be a Bubble?

- Experience Section: Lessons From Living Through Market Booms, Hype Cycles, and “This Time Is Different” Moments

- Conclusion

Note: This article is for educational and editorial purposes only. It is not financial advice, a stock recommendation, or a crystal ball wearing a Wall Street tie.

The stock market has been acting like it found an extra espresso shot in its morning coffee. Major U.S. indexes have pushed toward record highs, artificial intelligence stocks have attracted enormous investor attention, and corporate earnings have stayed surprisingly resilient despite sticky inflation, interest-rate uncertainty, and geopolitical noise. Naturally, investors are asking the question that appears every time prices rise faster than people can update their spreadsheets: Could the stock market boom be a bubble?

The honest answer is not as dramatic as cable-news graphics would like. The market does show some classic bubble-like symptoms: elevated valuations, heavy concentration in a narrow group of technology leaders, strong retail enthusiasm, and a popular story powerful enough to make cautious investors feel like they are missing the last helicopter out of Regret City. At the same time, the boom is not floating on pure imagination. Earnings are growing, AI investment is real, corporate profit margins remain strong, and large companies leading the rally are not tiny dot-com startups selling “future vibes” with a logo and a dream.

So the better question is not simply, “Is this a bubble?” It is: How much of today’s stock market boom is justified by fundamentals, and how much is priced for perfection? That is where the real story gets interesting.

What Is a Stock Market Bubble?

A stock market bubble happens when asset prices rise far beyond what underlying business fundamentals can reasonably support. In plain English, investors start paying filet-mignon prices for companies that may only be serving microwaved leftovers. Prices keep climbing because buyers expect other buyers to pay even more later. Eventually, expectations get too heavy for reality to carry, and the market corrects sharply.

Classic bubbles often share a few ingredients. First, there is a big new story: railroads, radio, the internet, housing, crypto, electric vehicles, or artificial intelligence. Second, there is easy access to money or a belief that liquidity will remain friendly. Third, there is social proof. Everyone seems to be getting rich, which is a very efficient way to make otherwise sensible people forget math. Finally, there is valuation expansion, where prices rise faster than earnings, cash flow, or sales.

Not every boom is a bubble. Sometimes markets rise because profits are rising, productivity is improving, and investors correctly anticipate a healthier economy. The difficulty is that bubbles usually look reasonable in the middle. They do not arrive wearing a name tag that says, “Hello, I am a historically dangerous valuation event.”

Why the Stock Market Is Booming

AI Is the Main Character

The biggest driver of the current market boom is artificial intelligence. AI has become more than a technology theme; it is now a market narrative, an earnings story, a capital-spending cycle, and a productivity bet rolled into one. The companies building AI infrastructuresemiconductors, cloud platforms, data centers, networking equipment, and software toolshave attracted huge investor interest because they appear to sit directly in the path of long-term economic change.

This matters because markets do not only price what companies are earning today. They also price what investors believe companies could earn tomorrow. If AI meaningfully improves productivity across health care, finance, manufacturing, logistics, education, energy, and software development, then today’s optimism may have a rational foundation. But if AI spending grows faster than AI profits, some valuations could start looking less like foresight and more like wishful thinking with a ticker symbol.

Earnings Have Been Stronger Than Expected

A bubble becomes much easier to argue when prices rise while earnings collapse. That is not the current setup. Analysts have expected solid S&P 500 earnings growth in 2026, with broad profit improvement projected beyond only the most famous technology giants. This is one reason many strategists remain constructive on U.S. equities even while acknowledging valuation risk.

Strong earnings do not eliminate bubble risk, but they change the conversation. A market trading at a high valuation because profits are accelerating is different from a market trading at a high valuation because investors have collectively decided that earnings are an outdated concept, like fax machines or quiet airports.

Investors Still Believe the Economy Can Hold Up

The U.S. economy has shown resilience despite higher borrowing costs, inflation pressure, and policy uncertainty. Employment has cooled at times but has not collapsed. Consumer spending has slowed in some areas but has not disappeared. Corporate America has also become remarkably good at protecting margins, passing along costs, and using technology to do more with less.

That resilience supports the bull case. If economic growth continues, inflation gradually cools, and corporate earnings rise, the market could keep advancing without automatically qualifying as a bubble. But that scenario requires a delicate balance. Investors are currently pricing in a lot of good news, and when a market is priced for a smooth landing, even a pothole can feel rude.

The Bubble Warning Signs Investors Are Watching

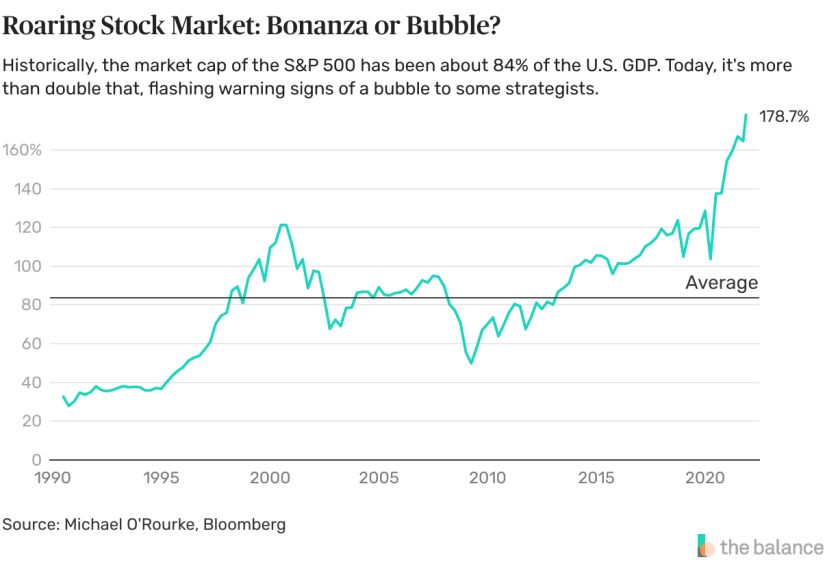

Valuations Are Elevated

One of the strongest arguments for caution is valuation. Traditional metrics such as the S&P 500 price-to-earnings ratio and the Shiller CAPE ratio have been high compared with long-term historical norms. High valuations do not predict an immediate crash, but they often reduce future return potential. Buying great businesses at stretched prices can still lead to disappointing results if expectations are already doing Olympic-level gymnastics.

The Shiller CAPE ratio is especially useful because it smooths earnings over a 10-year period, making it harder for one unusually strong year to make the market look cheap. When CAPE is elevated, investors are usually paying a premium for future growth. That premium can be justified, but only if the future shows up on schedule, wearing clean shoes and carrying profit margins.

Market Leadership Is Narrow

Another concern is concentration. A small group of mega-cap technology and AI-linked companies has contributed a large share of market gains. This does not automatically mean disaster. The largest companies today are highly profitable, globally dominant, and deeply embedded in the modern economy. Still, narrow leadership can make indexes more fragile. If a few giants stumble, the whole market can look wobbly even if hundreds of other companies are doing fine.

Think of it like a dinner table balanced on one very impressive leg. The leg may be made of titanium, polished by engineers, and admired by analysts. But it is still one leg.

AI Spending Must Eventually Produce AI Returns

The market is rewarding companies that benefit from AI infrastructure spending. That makes sense in the early phase of a technology buildout. The sellers of picks and shovels often profit before the miners find gold. But eventually, investors will ask whether the hundreds of billions of dollars being spent on chips, servers, cloud capacity, and data centers are producing enough revenue, productivity, and cash flow to justify the outlay.

This is where the AI boom could become vulnerable. If AI adoption spreads across industries and lifts margins, the rally may broaden. If companies spend heavily but struggle to monetize AI services, investors may begin repricing the entire theme. The technology can be revolutionary and still produce poor returns for overvalued stocks. The railroad changed America; not every railroad stock made investors rich.

Credit Markets Look Very Comfortable

Bubble risk is not only about stocks. Credit markets matter too. When corporate bond spreads are unusually tight, it suggests investors are not demanding much extra compensation for taking risk. Calm credit markets can support equities, but they can also signal complacency. In late-cycle environments, investors often become most relaxed shortly before risk wakes up from its nap and starts throwing furniture.

The Case That This Is Not a Bubble

The Leaders Are Real Businesses

One major difference between today’s market and the dot-com era is quality. Many leading AI and technology companies have enormous revenues, strong balance sheets, global customer bases, and substantial free cash flow. These are not companies built only on page views, chat-room excitement, and a business plan written during a caffeine emergency.

That matters. A market can be expensive without being a fantasy. Investors may be overpaying for quality, but overpaying for quality is not the same as buying companies with no path to profitability. Today’s largest tech leaders have real earnings, real products, and real competitive advantages.

Earnings Growth Is Broader Than One Stock

Although AI leaders dominate headlines, earnings growth expectations have started to include more sectors. Industrials, communication services, consumer discretionary companies, and even some old-economy businesses may benefit from AI adoption, automation, and productivity improvements. If market leadership broadens, the bubble argument weakens.

Broader participation is important because a healthier bull market usually does not rely on only one theme. If banks, manufacturers, health care companies, energy firms, software adopters, and smaller companies begin contributing to profit growth, the rally becomes less dependent on whether one chipmaker beats revenue estimates by a heroic amount.

Skepticism Still Exists

True bubbles often feature a dangerous shortage of doubt. In the late stages, anyone questioning the boom gets treated like someone who brought a salad to a pizza party. Today, skepticism is very much alive. Investors, analysts, and major institutions openly debate whether AI valuations are stretched, whether capital spending will earn adequate returns, and whether large-cap growth stocks can continue outperforming.

That skepticism can act as a stabilizer. Markets are more vulnerable when everyone agrees prices can only rise. The current environment has plenty of optimism, but it also has caution, rotation, and active debate. That does not guarantee safety, but it suggests the mood has not fully entered “gravity has been canceled” territory.

How Today Compares With Past Market Bubbles

The Dot-Com Bubble

The dot-com bubble of the late 1990s is the comparison everyone reaches for first, usually with the enthusiasm of someone finding an old yearbook photo. The similarity is obvious: a transformative technology, rapid valuation expansion, and investor excitement about a new economic era. The difference is that many dot-com companies had weak business models and little revenue. Today’s leading technology firms are much stronger financially.

However, the lesson of 2000 is not that all new technology is fake. The internet was real. The problem was that investors paid too much too soon for too many companies. AI may follow a similar pattern: real technology, real productivity, and possibly real overvaluation in selected areas.

The Housing Bubble

The housing bubble was different because it involved widespread leverage, complex credit products, and household balance sheets. Today’s equity market boom does not appear to have the same structure. Still, there is a shared lesson: when investors believe an asset class cannot fall much, risk management gets sloppy.

In stocks, leverage may appear through margin debt, options speculation, private credit exposure, or concentrated portfolios. The danger is not only that prices decline. The danger is that too many investors are positioned as if prices cannot decline.

The 2021 Speculation Wave

The 2021 boom in meme stocks, SPACs, unprofitable software, and crypto-related assets showed how quickly enthusiasm can reverse when rates rise and liquidity tightens. Compared with that period, today’s rally is more grounded in earnings and mega-cap profitability. But speculative behavior has not vanished. It has simply become more selective and better dressed.

What Could Pop the Bubble If There Is One?

Several catalysts could challenge the current stock market boom. The first is disappointing AI monetization. If companies cannot show a convincing return on AI spending, valuations in the sector could compress. The second is stubborn inflation. If inflation remains above target, the Federal Reserve may keep interest rates higher for longer, reducing the present value of future earnings. Growth stocks dislike high discount rates the way cats dislike baths.

A third risk is an earnings slowdown. High valuations become harder to defend if profit growth stalls. A fourth is geopolitical shock, including energy-price spikes, supply-chain disruptions, or trade-policy uncertainty. Finally, investor positioning itself can become a risk. When too many people crowd into the same trade, the exit door starts looking suspiciously narrow.

What Investors Should Watch Instead of Guessing

Trying to call the exact top of a market boom is a popular hobby with a terrible success rate. Instead, investors can watch practical indicators. Are earnings estimates rising or falling? Is market leadership broadening or narrowing? Are AI companies turning capital spending into measurable revenue and cash flow? Are credit spreads staying calm for good reasons or simply ignoring risk? Are valuations expanding because earnings are improving, or because investors are willing to pay more for the same profits?

Another useful signal is the behavior of equal-weighted indexes compared with market-cap-weighted indexes. If the equal-weighted S&P 500 starts catching up, it may indicate that the rally is becoming healthier. If only a handful of mega-cap stocks keep doing all the heavy lifting, the market may be more vulnerable than headline index levels suggest.

So, Could the Stock Market Boom Be a Bubble?

Yes, parts of it could be. That is the most balanced answer. The entire market does not need to be a bubble for some segments to be overpriced. AI infrastructure, mega-cap growth, speculative small caps, private technology valuations, and popular momentum trades may each carry different levels of risk.

The broader U.S. stock market boom appears to be supported by real earnings growth, genuine AI investment, and resilient economic activity. But the price investors are paying for that optimism is high. That means future returns may depend less on whether AI is important and more on whether AI becomes profitable fast enough to satisfy expectations already baked into stock prices.

In other words, the market may not be a cartoon bubble floating through the sky. It may be a very expensive hot-air balloon. It can keep rising if the fuel keeps burning. But passengers should probably know where the parachutes are.

Experience Section: Lessons From Living Through Market Booms, Hype Cycles, and “This Time Is Different” Moments

One of the most useful experiences investors can bring to a stock market boom is humility. Every major rally comes with a convincing story. During the internet boom, the story was that the web would change everything. That was true. During the housing boom, the story was that real estate was safe because people always need homes. That was partly true. During the AI boom, the story is that artificial intelligence can transform productivity, reduce costs, accelerate research, and create new business models. That may also be true. The trap is assuming that a true story automatically makes every stock price reasonable.

Experienced investors learn that the market can be right about the big idea and wrong about the price. The internet changed the world, but many internet stocks still collapsed. Electric vehicles reshaped the auto conversation, but not every EV-related company became a winner. Cloud computing was real, but investors still had to separate durable businesses from expensive promises. The same discipline applies to AI. A revolutionary technology does not cancel valuation, competition, debt, execution risk, or the possibility that profits arrive later than expected.

Another experience from past booms is that fear of missing out is one of the most expensive emotions in finance. It usually starts innocently. A friend mentions a stock. A headline says an index hit another record. A popular company rises 20% after earnings. Suddenly, sitting in a diversified portfolio feels boring, like bringing a library card to a fireworks show. But boredom is often underrated. Many long-term investors survive market cycles not because they perfectly predict bubbles, but because they avoid turning excitement into reckless concentration.

A practical lesson is to write down the reason for owning an investment before buying it. If the reason is “everyone is talking about it,” that is not analysis; that is peer pressure in a brokerage account. If the reason includes earnings growth, competitive advantage, balance-sheet strength, cash-flow potential, and a valuation that still makes sense under conservative assumptions, the decision is more grounded. This simple habit can prevent investors from confusing a good company with a good investment.

Market booms also teach the value of rebalancing. When one part of a portfolio rises dramatically, it can become a larger position than intended. Rebalancing does not require predicting a crash. It simply means returning risk to a level the investor can actually live with. Many people discover their true risk tolerance only after prices fall. Unfortunately, that is like discovering you cannot swim after jumping off the boat.

Finally, experienced investors understand that bubbles can last longer than skeptics expect. Being early to call a bubble can feel just as painful as being late to exit one. Prices can detach from fundamentals for months or even years. That is why all-or-nothing thinking is dangerous. The goal is not to shout “bubble” every time stocks rise or “new era” every time a technology improves. The goal is to stay flexible, respect data, diversify intelligently, and remember that markets reward patience more often than panic.

The current stock market boom may continue, correct, broaden, or split into winners and losers. No one knows the exact path. But investors who combine optimism about innovation with discipline about valuation are better prepared than those who bring only excitement. In a market where AI is the headline, earnings are the scoreboard, and valuation is the referee, the wisest approach is not fear or frenzy. It is informed cautionwith a sense of humor, because the market will always find new ways to humble anyone who claims to have it completely figured out.

Conclusion

The stock market boom could be a bubble in certain areas, especially where AI enthusiasm has pushed expectations far ahead of proven profits. But calling the entire market a bubble may be too simple. Strong earnings, real technology investment, and resilient economic growth give the rally a foundation that many past speculative manias lacked. Still, elevated valuations and narrow leadership mean investors should be careful, not careless.

The smartest takeaway is balanced: AI may be transformative, but price still matters. A great future can still produce weak investment returns if investors overpay for it today. The stock market does not need to crash for expectations to reset. Sometimes the bubble pops loudly; sometimes it simply leaks air while everyone pretends the balloon is still party-ready.