Table of Contents >> Show >> Hide

- What Carta’s Q1’22 Data Was Really Signaling

- The Macro Backdrop That Hit Venture in Q1’22

- How the Seed Market Changed on the Ground

- What Other Venture Data Sources Confirmed

- Why Q1’22 Was a Seed ShockNot a Seed Collapse

- What Founders and Operators Should Learn From This Quarter

- 500-Word Experience Notes From the Q1’22 Reset

- Conclusion

In startup years, Q1 2022 feels like a season finale: dramatic, expensive, and full of plot twists. One minute, founders were pitching in a market that rewarded speed and big narratives. The next, inflation was roaring, the Fed was raising rates, public tech stocks were sliding, and venture investors suddenly remembered the word “discipline.”

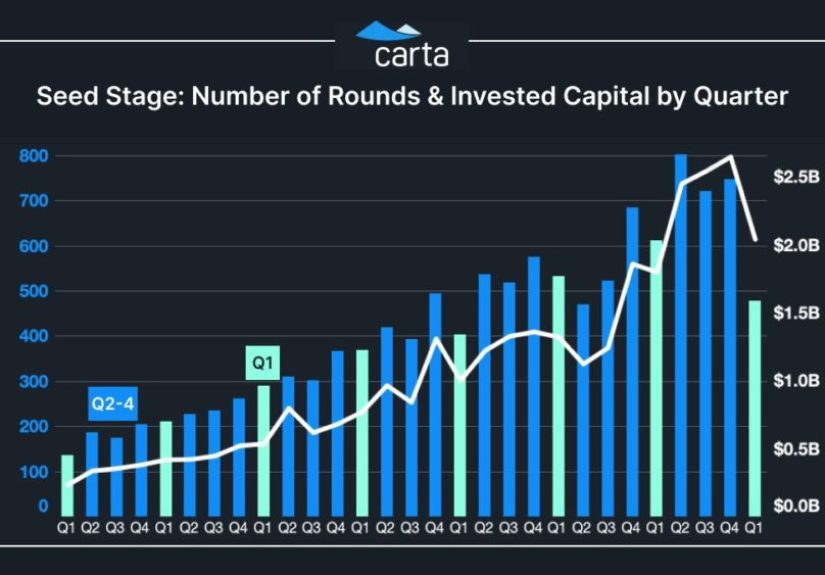

Carta’s data became one of the clearest signals of that shift. The headline that grabbed attention was simple but powerful: seed rounds were down more than 20% in Q1’22. And while seed proved more resilient than later stages, the change marked the beginning of a very different fundraising eraone defined by smaller checks, longer timelines, tougher diligence, and a lot more bridge rounds.

This article breaks down what happened, why it happened, and what it meant for founders, operators, and investors. We’ll also look at how the market evolved after the first shock, because the real story of Q1’22 is not just the dropit’s how everyone adapted once the easy-money music stopped.

What Carta’s Q1’22 Data Was Really Signaling

Carta’s Q1’22 private-market data showed a broad cooldown across startup fundraising. Deal volume fell sharply, and total cash raised dropped across multiple stages. Seed did not collapse the way later-stage venture did, but it clearly softened. That matters because seed usually acts like the “early warning sensor” of startup sentiment: when seed investors slow down, confidence is changing.

The phrase “seed rounds down more than 20%” captured a critical turning point. In practical terms, it meant fewer companies were getting funded at the earliest stage, and the bar to close a round was rising fast. Founders who had expected a quick process suddenly faced longer timelines, more investor meetings, and harder questions about burn, runway, and go-to-market strategy.

Carta’s own Q1 analysis also showed valuation pressure, especially beyond seed. Seed valuations dipped, but Series A and Series B felt stronger compression. That created a weird early-2022 dynamic: seed was still active, but everybody could see the storm heading toward the rest of the cap table.

Why seed looked “better” than later stages

Seed survived the first wave better than growth and late-stage rounds for one reason: early-stage investing is less tied to public-market comps. A pre-seed team with a strong product insight and a believable founder story can still attract capital even when SaaS multiples are tumbling. A late-stage company, on the other hand, gets marked against public comparables almost immediatelyand in 2022, that was painful.

In other words, seed investors can still dream. Growth investors have spreadsheets. In Q1’22, the spreadsheets won.

The Macro Backdrop That Hit Venture in Q1’22

Venture didn’t cool in a vacuum. The broader U.S. economy was sending warning flares in every direction. Inflation accelerated to levels not seen in decades, and the Federal Reserve began tightening policy. If 2021 was “money is cheap, build aggressively,” then 2022 became “capital has a cost now, please show your unit economics.”

Inflation changed investor behavior overnight

U.S. inflation hit 8.5% year over year in March 2022, the largest 12-month increase since 1981. That wasn’t just a headline for economistsit changed pricing assumptions, hiring plans, and valuation models. When inflation runs hot, investors demand higher returns. And when they demand higher returns, startup valuations tend to come down.

Founders felt this in subtle ways at first: more questions about margins, more scrutiny on growth efficiency, and less tolerance for “we’ll figure monetization out later.” The vibes were still startup-casual. The term sheets were not.

The Fed’s rate hikes hit startup math fast

The Fed raised rates in March 2022 and then again in May, including a larger move in early May. Those actions mattered to venture because they reset discount rates across the entire market. When rates rise, future cash flows are worth less in today’s dollars. That especially hurts high-growth companies whose value depends on what they might earn years from now.

In plain English: the “we’re growing fast, profits later” pitch became more expensive to finance.

Public markets cracked, and private markets followed

By April 2022, public tech stocks were already under heavy pressure. The Nasdaq posted its worst month since 2008, and broader equity markets sold off as investors anticipated more tightening and slower growth. Venture firms may invest in private companies, but they still watch the public market scoreboard. When public multiples fall, private valuations usually lagand then catch down.

That lag is exactly why Q1’22 was such a revealing quarter. The market had not fully reset yet, but the direction was clear.

How the Seed Market Changed on the Ground

The “down 20%” headline sounds like a top-down statistic, but the real impact showed up in day-to-day fundraising behavior. Founders started changing tactics. Investors changed pacing. Lawyers probably got fewer 1 a.m. “can we sign by tomorrow?” emails. (Probably.)

1) Fundraising cycles got longer

In hot markets, a strong founder can run a tight process and close quickly. In a cooling market, the same founder may need more meetings, more diligence, and more proof points. By late 2022, Carta data showed the time between rounds stretching dramatically, confirming what founders had already felt during the year: the clock got slower, but payroll did not.

This shift started showing up right after Q1. Investors were no longer optimizing for speed; they were optimizing for conviction. That may sound noble, but for founders with six months of runway, it feels more like cardio.

2) Seed investors favored cleaner stories

In 2021, many seed rounds closed on narrative momentum: huge markets, founder pedigree, and urgency. In 2022, those ingredients still helped, but investors increasingly wanted signals of traction and capital efficiency. Even at seed, teams that could show sharp customer demand, disciplined spend, and a credible roadmap stood out.

This did not mean every startup needed revenue on day one. It did mean investors became more selective about what “early” could excuse.

3) Round structures became more creative

As the market tightened, SAFEs, convertible notes, and bridge rounds became more common across early-stage financing. Some founders chose to extend runway without repricing. Some investors preferred smaller interim checks while waiting for clearer market conditions. The result was a rise in “not quite a new round, not quite a reset” financing structures.

This trend became even more visible in 2023 and beyond, when bridge rounds took up a bigger share of the early-stage ecosystem. Q1’22 didn’t invent the bridge round, but it definitely gave it a starring role.

What Other Venture Data Sources Confirmed

Carta wasn’t alone. Multiple U.S.-based venture and startup data sources showed the same broad pattern in early 2022: funding slowed, mega-rounds pulled back, and seed held up better than later stages (for a while).

Crunchbase: the slowdown was real, but seed stayed active first

Crunchbase’s Q1 2022 reporting showed global venture funding down quarter over quarter, with the biggest pullback in late-stage and technology-heavy segments. It also noted that seed remained comparatively strong in the early part of the reset. That lines up with the Carta narrative: seed was not immune, but it was more resilient than growth.

Crunchbase’s later seed-focused analysis is especially useful in hindsight. It showed that seed activity peaked around Q1 2022 and then trended down over the following quarters. So the Carta headline wasn’t just a one-quarter wobbleit was the start of a longer adjustment.

PitchBook/NVCA: U.S. deal value and exits cooled quickly

PitchBook and NVCA’s U.S. Venture Monitor data for Q1 2022 reinforced the market shift. U.S. venture deal value fell quarter over quarter, and exits slowed dramatically compared with the 2021 boom. That matters because exits feed the whole venture machine. When liquidity slows, investors get more cautious about new deploymenteven at seed.

The report also highlighted a changing deal environment by stage, including pressure on valuations and a more selective posture from investors. In other words, the slowdown wasn’t just fewer deals. It was a re-pricing of risk.

CB Insights and tech media: mega-round fatigue was spreading

CB Insights’ Q1 2022 venture coverage also pointed to a significant quarter-over-quarter decline in global funding and weaker mega-round activity. Around the same period, startup media reporting tracked the same pattern: the market was no longer rewarding “grow at all costs,” and investor attention shifted toward durability, not just speed.

Once mega-round appetite dropped, the psychology of the entire funding stack changed. Seed investors became more cautious because they knew the next round (Series A and beyond) might be harder to secure. And if the next round is harder, seed pricing has to adjust too.

Why Q1’22 Was a Seed ShockNot a Seed Collapse

It’s important to read the headline correctly. “Down more than 20%” sounds dramatic, and it was. But Q1’22 was not the end of seed investing. It was the end of easy seed investing.

In fact, Carta’s later data shows that seed remained a central part of venture activity even as Series A and later stages became more difficult. By 2023, the divergence was obvious: investors still liked getting in early, but they were much more cautious about paying up at the next institutional step. Seed became a safer place to hide relative to growth-stage chaos.

That created a new reality for founders:

- Seed was still possible, but not automatic.

- Story still mattered, but evidence mattered more.

- Valuation discussions became more grounded.

- Runway planning became a core fundraising strategy, not an afterthought.

If 2021 rewarded speed, 2022 rewarded stamina.

What Founders and Operators Should Learn From This Quarter

The biggest lesson from “seed rounds down more than 20%” is not “the market was bad.” Markets are always changing. The better lesson is this: the founders who survive resets are the ones who adapt their fundraising style as fast as they adapt their product.

Build your company so it can raise in two markets

Great startup teams plan for both a warm market and a cold market. In a warm market, they can accelerate. In a cold market, they can extend runway and still hit milestones. That means keeping enough flexibility in hiring, burn, and roadmap priorities to handle a slower fundraising cycle.

Q1’22 punished teams that assumed the 2021 market would last forever. It rewarded teams that treated fundraising as probabilistic, not guaranteed.

Metrics are a fundraising product

In tighter markets, founders often say, “Investors suddenly care about metrics.” The funny part is that investors always cared. In hot markets, they were just willing to tolerate more uncertainty. Q1’22 brought metrics back to the center of the room.

Even seed founders benefit from presenting a metrics narrative: customer demand signals, retention patterns, sales velocity, pilot conversion, or engagement depth. You do not need every KPI in the universe. You do need a clean answer to: “Why now, why you, and why this can compound?”

Don’t confuse bridge financing with failure

One of the healthier mindset shifts after Q1’22 was the normalization of bridge rounds and interim financings. A bridge is not a red flag by default. It can be a rational tool when the broader market is repricing and you need time to hit stronger milestones before raising a full-priced round.

The key is intentionality. A bridge round should buy time for a measurable improvement in the business, not just postpone hard decisions.

500-Word Experience Notes From the Q1’22 Reset

If you talk to founders who raised around Q1’22, a common theme comes up: the market changed faster than their internal planning cycle. Many started the quarter expecting a familiar processbuild a target list, run a tight pitch cadence, create some FOMO, close in a few weeks. Then reality stepped in wearing interest-rate hikes and a much grumpier public market.

One founder experience that showed up repeatedly was “meeting inflation.” Not the CPI report itself, but the startup version of inflation: cloud costs higher, hiring costs sticky, and customer buying decisions slower than expected. In 2021, some teams could absorb that with fresh capital. In 2022, the same teams had to explain how they would protect runway without freezing momentum. That led to more conversations about sequencingwhat to build now versus later, which hires were mission-critical, and what growth channels actually converted instead of merely looking cool in a deck.

Investors also describe Q1’22 as a quarter where they had to relearn pacing. In the hottest parts of 2021, some firms moved so fast that “diligence” occasionally looked like a speedrun. In Q1’22, many investors slowed down and reintroduced process: more customer calls, more partner debate, more skepticism around aggressive projections. From the founder side, that slowdown felt frustrating. From the investor side, it felt like returning to normal underwriting. Both things can be true at the same time.

Operators felt the shift too. Finance and people leaders inside startups suddenly had more influence because budgeting and headcount planning became central to fundraising narratives. A company with a strong product but messy planning often struggled to inspire confidence. Meanwhile, a team with moderate traction but crisp financial discipline could look surprisingly attractive. Q1’22 reminded everyone that fundraising is not only a founder function; it is an organizational signal.

Another experience that stands out is how communication changed. Before the reset, some startup updates focused heavily on top-line momentum and branding wins. After Q1’22, stronger teams began writing investor updates more like operating reports: what improved, what broke, what was learned, what changed, and what the company would do next. That style built trust. In uncertain markets, trust compounds almost as much as revenue.

Finally, there is the emotional side. Many founders interpreted the changing market as a verdict on their company when it was often a verdict on pricing conditions. That distinction matters. A harder fundraising market does not automatically mean a weak business. It usually means the burden of proof has increased. The founders who navigated Q1’22 best were often the ones who separated market conditions from company fundamentals, adjusted their strategy, and kept building. Less panic, more priorities. Fewer vanity milestones, more durable ones. Not as glamorous as a 2021-style blitz roundbut a much stronger foundation for the long game.

Conclusion

“Carta: Seed Rounds Down More Than 20% in Q1’22” is more than a historical headline. It marks the moment venture sentiment shifted from abundance to selectivity. Seed remained alive, but the rules changed: slower cycles, sharper diligence, tighter valuation discipline, and a stronger focus on runway and fundamentals.

The founders who adapted early treated the reset as a strategy problem, not a personal failure. They tightened operations, improved storytelling with real metrics, and raised with flexibility. That playbook still matters today. Markets will swing, but companies built for discipline tend to outlast companies built only for momentum.