Table of Contents >> Show >> Hide

- The Brain’s Cash Register: Why Money Feels Like Survival

- Scarcity Mode: When Your Wallet Hijacks Your Working Memory

- Stress, Cortisol, and the “Do Something!” Button

- Dopamine, Deals, and the Pleasure of Almost Getting Paid

- Losses Hurt, Gains Don’t Heal: The Emotional Asymmetry of Money

- Money and Happiness: The $75K Myth, the Update, and the Fine Print

- Financial Well-Being: The Goal Isn’t RichIt’s Secure and Free

- Make Money Less Weird: Brain-Friendly Habits That Actually Stick

- Conclusion: Spend Like a Mammal With a Spreadsheet

- Real-Life Experiences: “Your Brain on $” in the Wild (Extra )

Money isn’t just math. It’s a full-body, full-brain experiencecomplete with plot twists, drama, and that one impulsive purchase you swear was “basically an investment.”

The Brain’s Cash Register: Why Money Feels Like Survival

Let’s get one thing straight: your brain did not evolve in a world of credit scores, subscriptions, and “limited-time offers” that mysteriously reset every 24 hours. Your brain evolved in a world where resources meant survival. Food. Shelter. Safety. A tribe that didn’t leave you behind because you forgot to Venmo for the campsite.

So when modern life turns money into the universal remote control for everythingrent, healthcare, freedom, status, optionsyour brain treats it like a big deal. Not a “compare APRs” deal. A “we might die” deal. That’s why money can make otherwise rational adults act like raccoons fighting over a shiny object.

In the simplest terms, money is a proxy signal. When it feels stable, your brain gets a little more room to plan, reflect, and think long-term. When it feels threatened, your brain narrows its focus to right-now problems: “How do I get through this week?” The shift is subtle… until it isn’t.

Money hits three primal buttons

- Safety: Can I keep the lights on and my life intact?

- Control: Do I have choices, or am I stuck?

- Belonging/status: Am I “okay” compared to the people around me?

Those buttons are why money discussions can get weird fast. You think you’re arguing about groceries. Your nervous system thinks you’re arguing about survival.

Scarcity Mode: When Your Wallet Hijacks Your Working Memory

Ever notice how financial stress makes you feel… dumber? Like you can’t focus, can’t remember, can’t plan, and somehow you’ve opened the fridge eight times hoping it’ll contain “a solution” this time?

That’s not laziness or a character flaw. It’s bandwidth. When money is tightor even when it feels tightyour attention gets pulled toward urgent gaps: bills, deadlines, debt, and the creeping fear that one unexpected expense could flip the table.

Psychologists and behavioral researchers describe scarcity as a mindset that taxes cognitive resources. Your brain starts tunneling: you focus intensely on what’s missing, and everything else (long-term planning, comparison shopping, filling out annoying forms, remembering passwords) becomes harder. Scarcity doesn’t just change what you do. It changes what you can think about.

Why scarcity makes “bad” money choices feel inevitable

In scarcity mode, short-term relief becomes incredibly tempting. A payday loan. A credit card swipe. A “buy now, pay later” checkout. Not because you love debtbecause your brain is trying to reduce immediate pain. It’s like putting a bandage on a leak: it helps in the moment, but it can create new problems later.

This is also why financial “adulting” tasks can feel impossible when you’re stressed: calling the insurance company, negotiating a bill, switching providers, building a budget. Those tasks require executive functionplanning, working memory, self-controlexactly the stuff scarcity squeezes.

The cruel irony is that scarcity can increase the need for good decisions while reducing the mental fuel required to make them. It’s like asking someone to run a marathon while tightening their shoelaces.

Stress, Cortisol, and the “Do Something!” Button

Money stress isn’t just a thought. It’s biology. When your brain detects threat, it can kick off a stress response designed for predatorsnot overdraft fees. The stress system helps you react quickly. But it also changes how you evaluate risk, reward, and time.

Under acute stress, people tend to shift toward faster, more habitual decisions. Not necessarily smarter onesjust quicker ones. And chronic stress can reshape your patterns: more avoidance, more emotional spending, more “I’ll deal with it later” energy that somehow becomes a lifestyle.

How stress rewires financial decision-making

- Risk gets weird: stress can push you to play it too safe in some contexts and gamble in others (especially around losses).

- Time horizon shrinks: future-you becomes a stranger you mildly dislike.

- Habits take the wheel: you rely on default behaviors because they require less effort.

Cortisoloften called a “stress hormone”helps mobilize energy. That’s useful if you’re escaping danger. But if your danger is “my rent went up again,” living in high alert isn’t a flex. It’s exhausting. Over time, chronic stress is linked with problems like sleep disruption, anxiety, and difficulty focusingexactly the stuff that makes money management harder.

The hidden cost of financial stress

Financial stress can also create a feedback loop: stress worsens decisions, decisions create more financial mess, the mess increases stress. The loop can feel personal, but it’s often structural + biological + emotional, all holding hands like a very unhelpful group project.

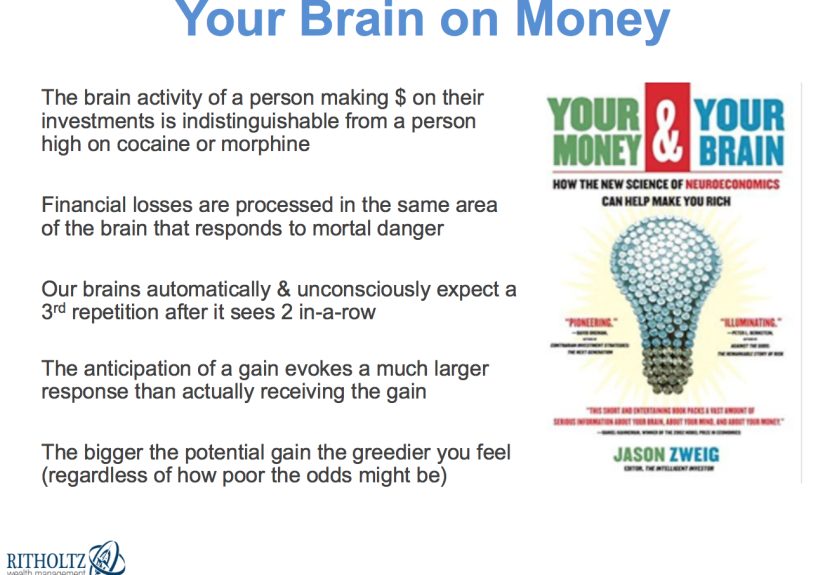

Dopamine, Deals, and the Pleasure of Almost Getting Paid

Here’s a spicy truth: your brain often gets more excited about anticipating rewards than actually receiving them. That’s why “maybe I’ll win” can feel electric, and why shopping can be thrilling right up until the delivery arrives and you realize you bought a fourth water bottle like you’re training for the hydration Olympics.

Researchers study reward circuitry using tasks built around monetary incentivesbecause money is a clean, powerful reward signal. Brain imaging studies often highlight regions like the ventral striatum (a key player in reward anticipation) lighting up when there’s a chance of gaining money. That anticipation is rocket fuel for motivation… and also for impulse spending.

Why discounts feel like victories

A sale doesn’t just reduce a price. It creates a story: “I outsmarted the system.” Your brain loves stories. A limited-time offer adds urgency. A countdown timer adds threat. Combine them and you’ve got a neurological cocktail that whispers, “Buy it now or regret it forever,” which is hilarious because the item is usually a lamp.

Why gambling and “lottery logic” are so sticky

Uncertain rewardslike jackpots or high-volatility betscan be uniquely compelling because the brain keeps leaning into possibility. It’s not just about winning; it’s about the mental movie of winning. That’s why people can chase losses even when the math is screaming, “Please stop.”

Losses Hurt, Gains Don’t Heal: The Emotional Asymmetry of Money

If you’ve ever lost $20 and felt personally insulted by the universe, but found $20 and felt only mildly pleased (for eight seconds), congratulations: you are human.

People tend to experience losses more intensely than equivalent gains. That asymmetry matters because modern money life is full of “loss-shaped” experiences: fees, price increases, surprise charges, medical bills, “your subscription is renewing” emails that arrive like tiny jump scares.

This is why some financial decisions are emotionally hard even when they’re logically correct. Selling an investment at a loss can feel like admitting failure. Cutting a lifestyle expense can feel like losing status or comfort. And negotiating salary can feel like social risk, even when it’s financially rational.

What your brain wants when money feels like loss

It wants relief. Certainty. Control. Sometimes it will pay extra for those feelingsthrough convenience fees, rushed decisions, or avoiding uncomfortable conversations. Recognizing that emotional goal (“I want relief”) helps you pick better tools than “just spend and hope.”

Money and Happiness: The $75K Myth, the Update, and the Fine Print

Money and happiness research is famous for one headline that refuses to retire: “Happiness tops out at $75,000.” That idea came from influential work distinguishing between life evaluation (how you rate your life overall) and emotional well-being (how you feel day to day). The original takeaway: life evaluation rises with income, while day-to-day emotional well-being seemed to level off around a certain point.

Later research complicated the story. More recent findings suggest happiness can continue rising with income beyond that level for many peopleespecially when higher income reduces stressors and increases a sense of control. There’s also nuance: some people remain unhappy even with more money, and for them income doesn’t provide the same boost. Translation: money can help, but it’s not a personality transplant.

The fine print your brain actually cares about

- Less stress buys more happiness than more stuff: reducing financial shocks and anxiety tends to matter a lot.

- Control is a huge mediator: money often helps most by increasing choicestime, safety, flexibility.

- Comparison is the happiness tax: if your “enough” depends on someone else’s highlight reel, your brain will never feel settled.

If you want a more useful question than “Does money buy happiness?” try: What problem is my money solving? Because “more money” is vague. “More money so I can sleep” is specificand your nervous system loves specific.

Financial Well-Being: The Goal Isn’t RichIt’s Secure and Free

A lot of people chase wealth when what they actually want is financial well-being: feeling secure and having freedom of choice. That can look different depending on your life. For one person, it’s building an emergency fund. For another, it’s reducing debt. For another, it’s finally having enough margin to say “no” to a job that’s eating their soul like a slow-moving piranha.

Financial well-being is less about a number and more about a state: stability in the present, resilience against shocks, and confidence about the future. When you aim at that, your money decisions get clearer because the goal is practicalnot performative.

Signals you’re moving toward financial well-being

- You can absorb a surprise expense without panic-spinning for three days.

- You can plan a month ahead without feeling like you’re predicting the weather with a spoon.

- You spend in alignment with your values more often than your emotions.

Make Money Less Weird: Brain-Friendly Habits That Actually Stick

Your brain loves defaults. It loves routines. It loves not having to make 400 micro-decisions a day. So the best money system isn’t the one with the prettiest spreadsheet. It’s the one that works when you’re tired, stressed, and one mildly rude email away from buying a “treat yourself” chair you do not have space for.

1) Automate the “good” stuff

If saving requires daily willpower, it won’t happen consistentlybecause willpower is a finite resource. Automate transfers to savings, retirement, and bill pay where possible. Make the healthiest option the easiest option.

2) Add friction to impulse spending

Remove saved cards from shopping apps. Use a 24-hour rule for non-essentials. Put wishlist items in a “cooling-off cart.” Friction gives your prefrontal cortex time to catch up and say, “We already own shoes.”

3) Reduce money decisions during peak stress

Don’t make big financial moves when you’re in fight-or-flight. If you’re panicking, your brain is optimizing for reliefnot accuracy. Set a rule: “No major financial decisions after 9 p.m.” (or after doomscrolling, whichever comes first).

4) Shrink the problem into next actions

Scarcity makes everything feel huge. Counter that with tiny steps: call one provider, set one payment plan, cancel one unused subscription, check one statement. Your brain calms down when it sees movement.

5) Talk about money like it’s normal (because it is)

Shame thrives in silence. But money is emotional for almost everyone. Talk to a trusted friend, partner, financial planner, or therapistespecially if anxiety or avoidance is driving your behavior. The goal is not perfection. It’s clarity.

Conclusion: Spend Like a Mammal With a Spreadsheet

“Your brain on $” is not a calm Excel wizard. It’s a survival-driven, reward-seeking, story-loving mammal that happens to have access to tap-to-pay.

When money feels scarce, your brain tunnels. When money feels threatening, your stress system grabs the steering wheel. When money feels exciting, reward circuits light up and whisper, “One more purchase won’t hurt,” like a tiny salesman living behind your eyeballs.

The win isn’t becoming a robot. The win is building a system that respects human wiring: automate what you can, reduce decision load, add smart friction, and aim for financial well-beingsecurity and freedom of choicerather than endless comparison. You don’t need to “out-discipline” your brain. You need to design around it.

Real-Life Experiences: “Your Brain on $” in the Wild (Extra )

Let’s take this out of the lab and into the place where your financial decisions actually happen: between errands, notifications, and that moment you open your banking app like you’re about to check exam results.

Experience #1: The Grocery Store Math Olympics

You walk in for “a few things” and immediately enter a competitive event you did not train for. Eggs cost what now? Your brain starts doing real-time trade-offs: brand vs. store brand, bulk vs. single, “Do we need snacks?” vs. “I deserve joy.” If money is tight, the mental load spikes fast. By aisle five, your brain is tired, and tired brains don’t make elegant decisionsthey make fast ones. That’s why you might overspend on convenience items or under-buy essentials and then make a second trip (which costs more time, more gas, more energy).

Experience #2: The Midnight Cart (a.k.a. Emotional Checkout)

It’s late. You’re drained. You’ve had a day. And suddenly that targeted ad feels like it understands you on a spiritual level. This is where “your brain on $” meets “your brain on stress.” Reward anticipation is high, self-control stamina is low, and buying something feels like a quick mood fix. The purchase gives a small hit of relief, then the next morning brings the hangover: regret, shame, or the classic “Wait… why did I buy an avocado slicer?”

The key insight isn’t “stop buying things.” It’s recognizing the pattern: you weren’t shopping for an objectyou were shopping for a feeling (comfort, control, novelty, distraction). Once you name the feeling, you can choose a cheaper way to meet it.

Experience #3: The Raise Conversation That Feels Like Skydiving

Negotiating salary often feels irrationally scary because your brain flags social rejection as threat. Even if the numbers make sense, your nervous system hears: “If they say no, I might be unsafe.” So people avoid the conversation, delay it, or accept less than they’re worth just to reduce discomfort. A helpful reframe is to treat it like a collaboration, not a confrontation: you’re discussing value, responsibilities, market rates, and next steps. Your brain relaxes when it sees a plan.

Experience #4: The Windfall That Doesn’t Fix Your Anxiety

Sometimes people get a bonus, tax refund, or unexpected cash and feel excited… and then oddly tense. Why? Because money can increase choices, and choices can increase pressure. Your brain may instantly start allocating: pay debt, invest, save, spend, help family, fix the car, upgrade your life, be responsible forever. That’s a lot. The move here is to pause and create categories: a portion for stability (emergency fund or bills), a portion for the future (debt payoff or investing), and a small portion for joy. Joy isn’t irresponsible; it’s a stress-buffer when it’s intentional.

Experience #5: The Quiet Relief of “Systems”

The most underrated “experience” is the moment your money life becomes boringin a good way. Bills get paid automatically. Savings happens without drama. You check your accounts and don’t flinch. That calm isn’t luck; it’s design. When your system carries the load, your brain gets its bandwidth back. And with bandwidth, you make better decisionsnot because you became a different person, but because your environment stopped constantly pushing your threat and reward buttons.

That’s the real takeaway of “Your Brain on $”: money isn’t just a tool you use. It’s a force your brain responds to. When you respect that response, you can build habits that feel less like punishment and more like peace.