Table of Contents >> Show >> Hide

- What “Fed-Created Recession” Actually Means (and What It Doesn’t)

- The Short Answer: 1981–82 Was the Classic “Fed-Induced” Downturn

- How We Got There: Stagflation, Energy Shocks, and a Credibility Hangover

- The Volcker Move: October 1979 and the “New Rules” Moment

- Rates Went Vertical (and the Economy Felt It Everywhere)

- Was It “Worth It”? The Case for (and Against) the Volcker Recession

- Why Later Fed Tightening Cycles Usually Don’t Qualify as “Creating a Recession”

- The Hidden Superpower (and Risk) of the Fed: Expectations

- How to Spot “Recession Risk” When the Fed Tightens

- So, What’s the Takeaway?

- FAQ: Quick Answers People Actually Google

- Experience Section: What It Feels Like When the Fed “Makes Money Expensive” (Real-World Lessons)

- 1) The shock arrives through monthly payments, not press conferences

- 2) Housing becomes a freeze frame

- 3) “Good businesses” can still fail if credit is the oxygen

- 4) Layoffs cluster, then cascade

- 5) People change their financial personality

- 6) Politics gets louder (and so does pressure on the Fed)

- 7) The “turn” is hard to timeeven for professionals

- 8) When inflation finally cools, it feels like exhaling after holding your breath

- 9) The biggest lesson people carry forward: debt structure matters

People love to say, “The Fed is going to cause a recession,” the way they say, “That one friend is going to

ruin brunch.” Sometimes it’s true. Sometimes it’s just vibes plus one scary chart on social media.

But there was a moment in modern U.S. history when the Federal Reserve tightened policy so hardand so

deliberatelythat “Fed-created recession” isn’t a hot take. It’s basically the consensus headline.

That moment was the early 1980s, when Paul Volcker’s Fed chose inflation’s throat over the economy’s comfort.

If you’ve ever wondered what it looks like when a central bank slams the brakes to put out an inflation fire,

this is the case study. It’s messy, painful, and (depending on your relationship with 18% mortgage rates)

mildly terrifying.

What “Fed-Created Recession” Actually Means (and What It Doesn’t)

Let’s define terms before the comment section shows up with pitchforks and Phillips Curves.

A “Fed-created recession” doesn’t mean the Fed wakes up one morning and says, “Let’s do a recession for fun.”

It means the Fed tightens monetary policy (raising interest rates and/or restricting liquidity)

enough that a downturn becomes the likely, even accepted, cost of restoring price stability.

In most recessions, multiple culprits are involved: oil shocks, financial crises, pandemics, policy mistakes,

global chaos, bad luck, and yessometimes the Fed stepping on the economy’s shoelaces. The early 1980s stand out

because tight money wasn’t just in the mix; it was a primary driver.

The Short Answer: 1981–82 Was the Classic “Fed-Induced” Downturn

The recession most often described as “created” (or “engineered,” or “induced”) by the Federal Reserve is the

July 1981 to November 1982 recessioncommonly called the Volcker recession.

It followed closely after a shorter 1980 recession, creating a brutal one-two punch for households and

businesses.

The key point isn’t that the Fed accidentally tripped the economy. The key point is that the Fed tightened

to break entrenched inflationand the recession was the (grimly) predictable result.

How We Got There: Stagflation, Energy Shocks, and a Credibility Hangover

By the late 1970s, the U.S. economy had a problem cocktail: slow growth, high unemployment at times,

and inflation that kept coming back like a sequel nobody asked for. The public’s faith that inflation would

return to normal “soon” was eroding. That matters because inflation isn’t just a numberit’s a social habit.

If everyone expects prices and wages to rise fast, they behave in ways that help make it true.

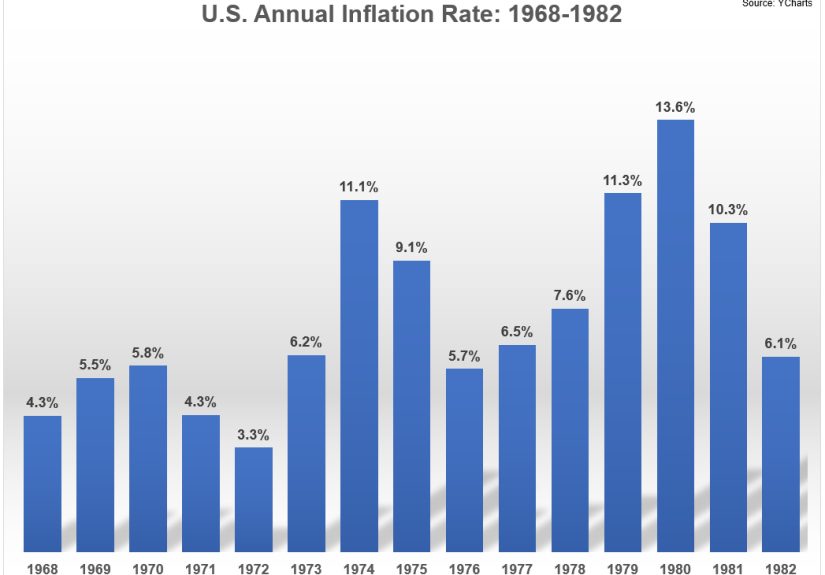

Inflation wasn’t just highit was persistent

Consumer prices surged in 1979 and 1980, driven heavily by food and energy, among other components.

When inflation hangs around long enough, it stops feeling “temporary” and starts feeling like the weather.

And fighting it requires more than polite nudges.

The Fed’s big fear: losing the plot

The Fed’s job, by law, is to pursue maximum employment and stable prices (often summarized as the “dual mandate”).

But in the late 1970s, it looked like the “stable prices” part had wandered off into the woods.

Restoring credibilityconvincing everyone the Fed would do what it takesbecame the mission.

The Volcker Move: October 1979 and the “New Rules” Moment

When Paul Volcker took the helm in 1979, the Fed shifted into a more aggressive anti-inflation stance.

In October 1979, the Fed announced measures aimed at reining in inflation, including a shift in operating

procedures that emphasized controlling the growth of money and bank reserves more directly.

Translation: instead of treating interest rates like a thermostat you adjust gently, the Fed treated inflation

like a house fire and grabbed the biggest hose in the station. The result was a period of very high and very

volatile interest ratesexactly the kind of environment that punishes borrowing, cools demand, and can tip

the economy into recession.

Rates Went Vertical (and the Economy Felt It Everywhere)

Tight monetary policy works through a simple chain reaction:

higher short-term rates → higher borrowing costs → less spending and investment → slower growth → fewer jobs.

In the early 1980s, that chain reaction wasn’t subtle. It was loud. It was immediate. It was wearing steel-toed

boots.

Housing: the first domino

Housing is famously interest-rate sensitive. When mortgage rates soar, buyers vanish, construction slows,

and related industries (materials, furnishings, appliances) feel the chill. In 1981, 30-year fixed mortgage

rates reached eye-watering highsnumbers that make modern homebuyers clutch their spreadsheets and whisper,

“Nope.”

Manufacturing and autos: the next dominoes

Big-ticket goodscars, machines, durable equipmentare also rate-sensitive. Higher financing costs shrink

demand, squeeze margins, and push firms to cut production and jobs. During the 1981–82 downturn, job losses

hit widely, with manufacturing, construction, and autos particularly affected.

The labor market: the painful scoreboard

By late 1982, unemployment had reached postwar-record territory. This is where the “Fed created a recession”

argument becomes emotionally real: the disinflation worked, but it worked by putting millions of people out of

work in the short run.

Was It “Worth It”? The Case for (and Against) the Volcker Recession

You can’t talk about the Volcker recession without confronting the moral math: how many points of inflation are

“worth” how many points of unemployment? There’s no clean answerjust tradeoffs, politics, and history.

The case for: credibility is a long-term asset

Many economists argue the Volcker disinflation reset inflation expectations and laid groundwork for decades of

lower inflation. If households and businesses believe the Fed will keep inflation low, wage and price setting

behavior changes. The economy can grow without constantly re-igniting an inflation spiral.

The case against: the burden was uneven

Recessions don’t distribute pain fairly. Interest-rate shocks hammer borrowers, new homebuyers, small

businesses, and workers in cyclical industries first. Meanwhile, anyone holding cash or short-duration assets

might quietly enjoy higher yields. That’s not a “gotcha.” It’s just how the transmission mechanism works.

Why Later Fed Tightening Cycles Usually Don’t Qualify as “Creating a Recession”

The Fed has tightened plenty of times since the early 1980s. But most later downturns were driven by a mix of

forces where the Fed was a contributor, not the starring villain in the credits.

1994–95: the famous soft landing

A classic counterexample is the mid-1990s, when the Fed tightened under Alan Greenspan and the economy avoided

a recessionoften cited as a “soft landing.” This episode is why economists keep hope alive the way sports fans

keep hope alive: irrationally, but with a few historical highlights.

2004–06: tightening into a financial bubble era

The mid-2000s tightening cycle is still debated. Some argue rates were too low for too long early on, fueling

risk-taking; others emphasize regulation, mortgage-market structure, and leverage as the key drivers of the

eventual financial crisis. Either way, the Great Recession wasn’t a clean “Fed cranked rates, recession happened”

story the way 1981–82 was.

The Hidden Superpower (and Risk) of the Fed: Expectations

Monetary policy isn’t only about today’s rate. It’s also about what people think the Fed will do nextand what

they think inflation will be next year, and the year after that. When credibility is strong, the Fed can do less

to achieve more. When credibility is weak, the Fed may need to do more to be believed.

In the Volcker era, restoring credibility required a dramatic demonstration. Painful? Yes. Effective at changing

beliefs? Also yes. That’s the central irony: the Fed’s gentler tools work best when people trust them.

How to Spot “Recession Risk” When the Fed Tightens

No single indicator is magic. But historically, a few signals tend to show up when monetary tightening becomes

recession-threatening.

1) The yield curve gets weird

When short-term interest rates rise above long-term ratesan “inverted” yield curvemarkets are often signaling

that policy is tight enough to slow growth substantially. This has a notable track record as a recession signal,

though it’s not infallible and can be distorted by other forces.

2) Interest-sensitive sectors crack first

Watch housing permits, home sales, auto sales, and business investment. These are usually the early-warning

systems because they’re funded with credit. When credit gets expensive, activity drops.

3) The job market turns from “hot” to “huh?”

Unemployment is often a lagging indicator, but layoffs in cyclical industries can show up earlier. If hiring

freezes spread and job openings fall quickly, recession risk rises.

So, What’s the Takeaway?

The last time the Fed clearly “created” a recessionthe kind where tight monetary policy was the main eventwas

the 1981–82 Volcker recession. The Fed tightened aggressively to crush entrenched inflation, and

the economy contracted hard as a result.

The lesson isn’t “the Fed always causes recessions.” The lesson is that when inflation becomes deeply embedded,

getting rid of it can require restrictive policy that risks (or even accepts) a downturn. If you want a painless

disinflation, history suggests you’re shopping in the “rare collectibles” aisle.

FAQ: Quick Answers People Actually Google

Did the Fed intentionally cause the 1981–82 recession?

The Fed intentionally tightened to defeat inflation; the resulting recession is widely viewed as a consequence

of that tight policy. “Intentional recession” is too strong for some historians, but “recession accepted as a

cost” is hard to dispute.

Was the 1980 recession also Fed-created?

The 1980 recession had multiple factors, including credit controls and tight policy. The early 1980s are often

discussed as a two-recession sequence tied to the broader disinflation campaign.

What’s the best modern comparison?

Comparisons usually look at periods where inflation surged and the Fed tightened quickly. But the structure of

mortgages, corporate debt, banking, and global finance has changed a lot since 1981so the transmission can look

different even if the playbook rhymes.

Experience Section: What It Feels Like When the Fed “Makes Money Expensive” (Real-World Lessons)

You don’t need a PhD to understand a Fed-induced recession. You just need to try refinancing a mortgage when rates

have launched into the stratosphereor run a business that depends on customers financing big purchases. Below are

experience-based observations (the kind people, firms, and communities repeatedly report during hard tightening

cycles), using the Volcker era as the clearest reference point.

1) The shock arrives through monthly payments, not press conferences

Most people didn’t experience the early 1980s as an abstract “fight against inflation.” They experienced it as:

“My loan payment just exploded,” “The bank said no,” or “The house we wanted is suddenly impossible.”

Monetary policy becomes real the moment a payment quote changes your life plan.

2) Housing becomes a freeze frame

When mortgage rates surge, housing markets can stall like someone hit pause. Buyers step back, sellers cling to

old price expectations, and construction firms face a pipeline that dries up. Even people who aren’t moving feel

the effects: fewer renovations, fewer furniture purchases, fewer “let’s upgrade the car too” decisions. It’s a

chain reaction that spreads across local economies.

3) “Good businesses” can still fail if credit is the oxygen

Small and mid-sized firms often rely on lines of credit to manage inventory and payrollespecially in seasonal

industries. When rates rise fast, the cost of carrying inventory rises, lenders tighten standards, and cash flow

becomes a daily stress test. During severe tightening, you can see otherwise competent businesses shrink or close

simply because the financing environment turns hostile.

4) Layoffs cluster, then cascade

In rate-driven downturns, layoffs typically cluster first in interest-sensitive sectors: construction, autos,

manufacturing, and suppliers. Then the cascade begins: fewer paychecks in the community means weaker demand for

restaurants, retail, services, and local contractors. A “factory slowdown” becomes a “Main Street slowdown.”

5) People change their financial personality

High inflation encourages “spend now” behavior because money loses purchasing power quickly. High rates flip the

script: savings accounts and safe bonds finally pay something meaningful, and consumers become more cautious.

Psychologically, the economy shifts from “growth at all costs” to “don’t get caught out.” That mindset shift

can be stabilizing long-term, but it can also deepen a short-term slump.

6) Politics gets louder (and so does pressure on the Fed)

In the Volcker era, unemployment and business pain generated intense political pressure. That’s a consistent

experience: when job losses mount, the Fed’s independence stops being a civics lesson and starts being a national

argument. People want reliefand they want it fast.

7) The “turn” is hard to timeeven for professionals

Another repeated experience: nobody rings a bell at the top of rates. Businesses delay investment too long or

cut too aggressively; households wait for “a better deal” that arrives after the opportunity has passed. Markets

swing between panic and relief. If severe tightening teaches anything, it’s humility: even smart people can’t

precisely time when policy goes from restrictive to recessionary to easing.

8) When inflation finally cools, it feels like exhaling after holding your breath

The irony of a harsh disinflation is that its benefits are quiet. Prices don’t “go back” to old levels; they just

stop accelerating as fast. But stable prices make long-term planning possible again. Wage negotiations become less

frantic. Businesses can budget without assuming chaos. The relief is subtlebut it’s real.

9) The biggest lesson people carry forward: debt structure matters

One of the most practical takeaways from the Volcker era is that how you borrow can matter as much

as how much you borrow. Fixed-rate vs. variable-rate debt, short-term refinancing needs, and cash

buffers can determine who survives a rate shock. In other words: in a world where the Fed can turn the price of

money up quickly, resilience is often built in the boring years, not the dramatic ones.

Put all that together and you get the lived reality behind the phrase “Fed-created recession.” It’s not a slogan.

It’s a story of payments, hiring decisions, canceled projects, and communities adapting in real time. The Volcker

recession is remembered not because central banks enjoy inflicting painbut because it shows what happens when

inflation gets so entrenched that restoring stability requires a deliberately restrictive stance.