Table of Contents >> Show >> Hide

- The hard truth: uncertainty is permanent, not a phase

- Volatility isn’t a sign you’re doing it wrongit’s the entry fee

- Diversification: the strategy that always feels broken

- Timing the market is seductiveand brutally expensive

- The behavior gap: your portfolio isn’t the biggest threatyou are

- What acceptance actually looks like: a plan built for real life

- Experiences related to “Something Most Investors Simply Cannot Accept”

- Conclusion: acceptance is a competitive advantage

Investors love certainty the way toddlers love the word “mine.” We want tidy stories, clean timelines, and charts that only go up and to the right. But markets

are not a math worksheet. They’re more like a group chat: noisy, emotional, occasionally irrational, and guaranteed to surprise you at the worst possible time.

Here’s the thing most investors simply cannot accept: uncertainty isn’t a temporary glitch in the marketit’s the product. The market doesn’t

pay you for being brave in the abstract. It pays you (over time) for tolerating ambiguity, for holding through uncomfortable periods, and for resisting the

deeply human urge to “do something” precisely when doing something is most likely to be a mistake.

If that sounds unfair, congratulationsyou’re reading an investing article. Let’s talk about what this truth actually means, why it’s so hard to swallow,

and how to build a strategy that doesn’t collapse the moment headlines get dramatic.

The hard truth: uncertainty is permanent, not a phase

Markets pay for uncertainty, not effort

You can work hard, research deeply, and create a color-coded spreadsheet that would make an engineer weep with joyand the market can still humble you by

lunchtime. That’s not because research is useless. It’s because markets reflect millions of competing opinions, constantly updated with new information.

What you call “risk” is often just “the future refusing to RSVP.”

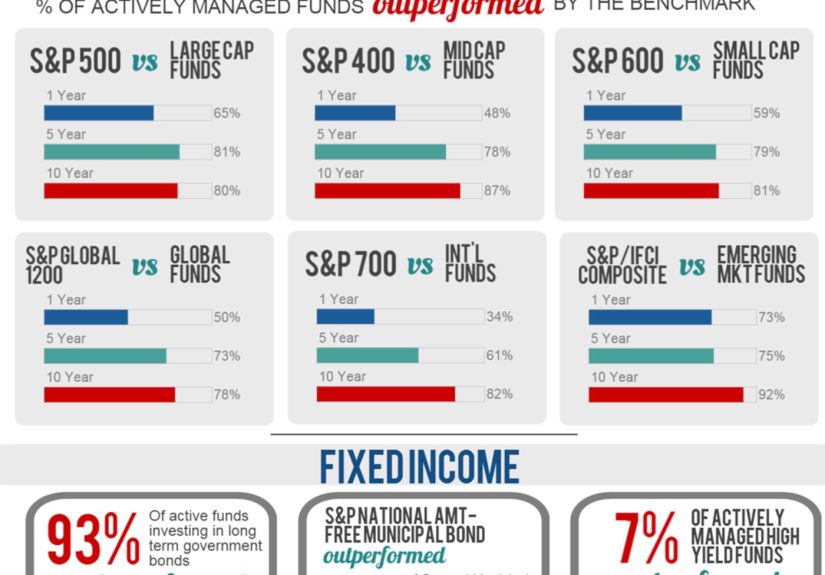

This is why broad U.S. stocks have historically offered higher long-run returns than cash-like options: you’re bearing more uncertainty along the way. For

example, the S&P 500often treated as a stand-in for large U.S. companiescovers about 80% of available U.S. market capitalization, yet its path is

anything but smooth. It’s big, diversified, and still perfectly capable of scaring the confidence out of a room.

“Normal” includes drawdowns

Many investors say they can handle volatilityuntil volatility shows up and starts doing volatility things. They picture a “bad year” as a mild dip, like

spilling coffee on your desk. Markets, however, sometimes behave like a toddler with finger paint: chaos is not just possible; it’s part of the experience.

J.P. Morgan’s long-running “Guide to the Markets” highlights a reality that shocks people every time: even in years that finish positive, the market often

experiences meaningful drops during the year. In one widely shared chart, the average intra-year decline is around the mid-teens, yet many years still end

with gains. Translation: the market can feel terrible on the way to being fine.

Volatility isn’t a sign you’re doing it wrongit’s the entry fee

Corrections and sell-offs are common

Investors tend to treat a 10% drop like a fire alarm. Historically, it’s more like thunder: loud, unsettling, and not unusual. Financial media will call it

a “correction,” your group chat will call it “the end,” and your brain will call it “get me out of here.”

The tough acceptance is this: market declines are not proof that investing stopped working. They are part of how markets price risk in

real timereacting to earnings, interest rates, inflation expectations, geopolitical shocks, new technologies, policy changes, and plain old fear.

The market doesn’t offer a comfort refund

A lot of people secretly expect the market to be “fair” in the moment: “I invested responsibly, so why is my account down?” Markets don’t grade on effort.

They grade on exposure. If you want the long-term potential of stocks, you also get the short-term mood swingsno opt-out checkbox.

This is why “risk tolerance” isn’t a personality quiz; it’s a design requirement. The SEC’s investor education materials emphasize that time horizon matters:

if you need money soon, volatility can be dangerous; if your horizon is longer, you may be able to ride through ups and downs without forcing bad decisions.

Diversification: the strategy that always feels broken

If everything is winning, you’re probably not diversified

Diversification is often sold like a magic shield. In reality, it’s more like a seat belt: it doesn’t prevent accidents; it prevents the accident from

ruining your life. A diversified portfolio will always contain something that looks stupid at any given timebecause different assets take turns

leading and lagging.

Investor.gov describes diversification and asset allocation as core risk-management ideas: spread exposure across categories (like stocks, bonds, and cash),

then rebalance over time. The goal isn’t to win every year. The goal is to avoid catastrophic outcomes and to stay in the game long enough for compounding

to matter.

The emotional cost: you must hold the “boring” parts

Many investors abandon diversification because it’s emotionally unsatisfying. They’d rather own the one thing that’s “working” right now. That’s a

completely human impulseand a common way to buy high, sell low, and repeat the process until your patience files for divorce.

Timing the market is seductiveand brutally expensive

Missing the best days can do real damage

One of the most consistent findings across major firms is that trying to jump in and out of the market can backfire because strong up days often cluster

near scary down days. Charles Schwab’s research shows that being out of the market for just a small number of top-performing days over long periods can

materially reduce returns. BlackRock and other large asset managers illustrate similar patterns: the cost of “waiting for clarity” can be the loss of the

very rebounds that drive long-term performance.

Here’s the irony investors hate: you usually feel most confident after prices have risen, and most fearful after prices have fallen.

Market timing asks you to do the opposite of what your nervous system wants. That’s why it’s so hardand why “I’ll get back in when things settle down”

often turns into “I guess I missed it.”

The market’s best and worst days can be neighbors

Financial reporting has repeatedly noted that extreme moves tend to arrive in clusters. Big down days can be followed quickly by big up days. This makes

all-or-nothing decisions risky: if you step aside to avoid pain, you may also step aside from the recovery.

The behavior gap: your portfolio isn’t the biggest threatyou are

Loss aversion is powerful (and very normal)

Behavioral finance has a brutally simple message: people hate losses more than they enjoy equivalent gains. Prospect theorypopularized by the work of

Daniel Kahneman and Amos Tversky and widely explained in mainstream investing educationhelps describe why a portfolio decline can feel like a personal

insult rather than a statistical event.

That emotional punch leads to predictable patterns: panic selling, performance chasing, and the “disposition effect” (selling winners too soon while

holding losers too long). None of these behaviors require low intelligence. They require only that you be a human with a pulse and Wi-Fi.

Investor returns often lag the investments they own

This is the part that stings: research and industry analysis frequently show that the average investor’s realized results can trail the returns of the

funds or markets they invest in, largely due to poorly timed decisions. DALBAR’s long-running investor behavior work is frequently cited for documenting

how buying, selling, and switching during emotional periods can reduce outcomes. Morningstar has also highlighted “investor return” gapswhere the dollar-

weighted return investors receive is lower than a fund’s reported total return because people tend to add money after performance and withdraw after pain.

In other words, it’s possible to own “good investments” and still get “bad results” if your behavior is out of sync with your plan.

What acceptance actually looks like: a plan built for real life

1) Decide what you’re investing for (and when you’ll need it)

Your time horizon is the steering wheel. Money needed soon shouldn’t be forced to ride a roller coaster. Money for long-term goals can usually tolerate

more volatility because it has time to recover. This is basic, unsexy planningand it’s the difference between “temporary drawdown” and “permanent

mistake.”

2) Use asset allocation as your stress management system

Asset allocation is not about predicting what will win next. It’s about choosing a mix you can stick with. Investor.gov and SEC educational materials

emphasize diversification and rebalancing as ways to manage risk. Rebalancingperiodically returning to your target mixcan also automate “buy low, sell

high” behavior without requiring superhuman willpower.

3) Automate the good decisions

If your plan relies on you being calm every day forever, it is not a plan. It’s a motivational poster. Consider systematic contributions (like investing a

set amount on a schedule) so progress doesn’t depend on market mood. Fidelity’s investor education content, among others, encourages disciplined investing

during volatilitybecause the hardest moments are often the ones that later look like opportunities.

4) Minimize the controllables: fees, taxes, and churn

You can’t control next quarter’s market return. You can control costs and behavior. Lower fees and less unnecessary trading keep more of your return. If

two strategies are similar, the cheaper and simpler one often wins the real-world contest because it’s easier to maintain.

5) Define rules for “headline emergencies”

Most emotional investing mistakes happen during breaking news. So write rules before you need them. Examples:

- If the market drops sharply, I wait 72 hours before making changes.

- I rebalance on a calendar schedule, not based on fear.

- I do not raise risk because something is trending, and I do not drop risk because something is scary.

The goal isn’t to remove emotion. The goal is to keep emotion from driving the car.

Experiences related to “Something Most Investors Simply Cannot Accept”

Below are a few real-to-life experiencescomposite stories drawn from common investor patternsthat show how this acceptance problem plays out in practice.

No unicorns, no secret indicators, and no “I doubled my money in a week” fairy tales. Just ordinary humans trying to invest while also living their lives.

Experience #1: The “I’ll wait until things feel safe” loop

One investor (let’s call her Maya) built up cash for years because she wanted to invest “when the market calms down.” The problem was that “calm” kept

moving. When markets rose steadily, she felt it was “too late.” When markets fell, she felt it was “too risky.” So she waitedthrough rallies, through

pullbacks, through recoveriesuntil years passed and her cash did exactly what cash does: it sat there looking stable while inflation quietly chewed on its

purchasing power.

The turning point wasn’t a hot stock tip. It was accepting that safety is not an on/off switch you can time. Maya set a simple schedule: invest a fixed

amount each month into a diversified mix. She didn’t feel brave on day one. She felt annoyed that she couldn’t find the “perfect time.” But within a year,

she noticed something bigger than returns: her anxiety dropped because the decision was no longer daily. The plan was doing the work. The market was still

unpredictable, but her behavior became predictableand that’s the kind of predictability investors actually need.

Experience #2: The diversification disappointment (a.k.a. “Why do I own the loser?”)

Another investor, Jordan, built a portfolio with both stocks and bonds. When stocks surged, bonds lagged. Jordan felt foolish for owning the “slow” asset

and considered selling it to buy more of what was hot. Later, when stocks stumbled, bonds helped reduce the portfolio’s overall decline. Suddenly, Jordan

was grateful for the same “boring” allocation he almost abandoned.

The lesson Jordan learned is the one investors resist most: diversification rarely looks brilliant in the moment. It looks like compromise. It feels like

owning umbrellas on sunny days. But it’s designed for the day you don’t want to imaginebecause that’s exactly when you’ll need it.

Experience #3: The panic-sell scar and the rebound regret

Then there’s Sam, who invested for retirement and felt confident until the market dropped sharply. Sam watched the account fall day after day and finally

sold to “stop the bleeding.” The sale brought temporary reliefuntil the market rebounded and Sam realized the next problem: getting back in felt even

harder. Prices were higher, headlines were optimistic again, and Sam felt like he’d missed the recovery. The regret didn’t come from the drop. It came from

the reaction to the drop.

Sam eventually rebuilt confidence through two changes: (1) he reduced risk to a level he could actually hold through downturns, and (2) he created a simple

rebalancing rule so decisions weren’t made in the heat of fear. He learned that courage is not white-knuckling a portfolio that keeps you up at night.

Courage is building a portfolio you can stay withbecause the only way compounding works is if you remain invested long enough to let it happen.

Conclusion: acceptance is a competitive advantage

The market will never make it easy to be a long-term investor. It will offer you uncertainty, volatility, and the occasional emotional gut check. The

uncomfortable truthwhat most investors cannot acceptis that those rough edges are not defects. They are the price of admission for the

potential of long-term growth.

Accept uncertainty. Design for it. Automate what you can. Diversify even when it feels awkward. And remember: the goal isn’t to predict the futureit’s to

build a plan that survives it.

Educational note: This article is for general information, not personalized financial advice. Consider a qualified professional for decisions tied to your situation.