Table of Contents >> Show >> Hide

- The physician story behind the headline

- What they actually did to pay off $100,000 so fast

- Why this strategy worked so well

- Could another physician do this today?

- The debt payoff blueprint physicians can borrow from this story

- How physicians can create extra payoff power

- The mistakes that keep physicians in debt longer than necessary

- What this payoff story really teaches

- Additional physician experiences that prove this is not a one-off miracle

- Conclusion

There are two kinds of doctor money. The first kind lives in spreadsheets, job offer letters, and compensation reports. The second kind mysteriously disappears into daycare, taxes, housing, groceries, insurance, and that “tiny treat” called a car payment. This story is about what happens when a physician stops pretending those two kinds of money are the same thing and starts treating debt payoff like a medical emergency instead of a vague New Year’s resolution.

The headline sounds almost cartoonish: $100,000 paid off in six months. It feels like the sort of thing that should come with a suspiciously enthusiastic infomercial host and a bonus set of steak knives. But the truth is far less glamorous and much more useful. This physician did not stumble upon a magic budgeting app, marry a hedge fund, or discover a secret room behind the hospital cafeteria filled with gold bars. She used a brutally simple mix of lifestyle cuts, refinancing, targeted monthly payments, windfalls, and consistent behavior. In other words, she used a plan.

And that is exactly why this story matters. It is not impressive because it is flashy. It is impressive because it is repeatable.

The physician story behind the headline

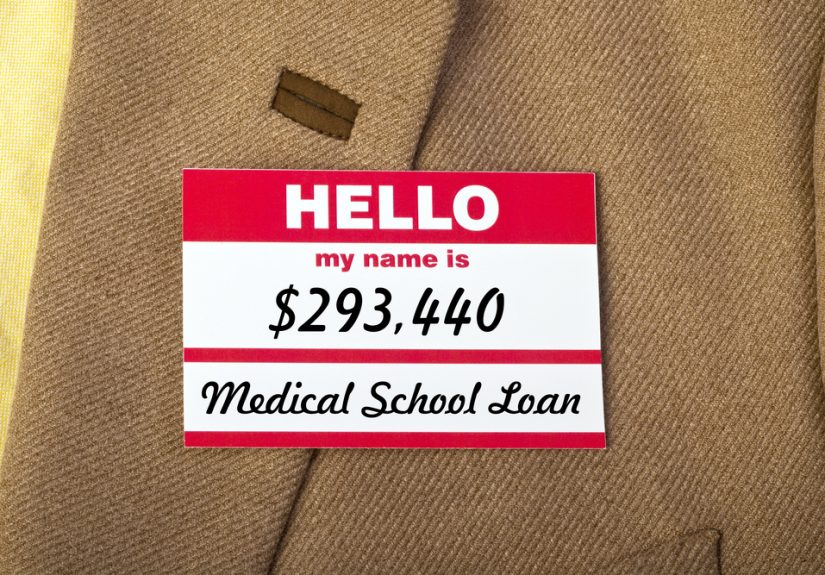

The physician at the center of this story first shared her experience publicly after realizing that her debt had become a major source of stress. She entered medical school with no college loans, but borrowed about $191,000 for medical school. A year away from school, combined with loan forbearance and capitalized interest, made the balance worse. During residency, income-based payments kept the account alive but did little to seriously reduce the principal. By the time she was practicing as an attending, the student loan balance had grown to about $237,000.

That was not the only debt in the picture. There was also mortgage debt, car debt, and another housing-related loan tied to a rental property. Altogether, her household sat under roughly three-quarters of a million dollars in total debt. On paper, everything looked respectable. Bills were paid. Credit was strong. The family looked successful. But emotionally, financially, and mentally, the arrangement was exhausting.

That tension is the real plot twist in many physician debt stories. The issue is not always low income. Quite often, it is high income paired with high fixed costs. Once every dollar has a job, the salary stops feeling large and starts feeling decorative.

The turning point came when this household stopped defending its lifestyle and started interrogating it. A totaled vehicle created a chance to upgrade, but instead of financing another shiny car, they bought a used replacement with cash. Then came a bigger decision: they moved, rented modestly instead of buying again, and intentionally “deflated” their lifestyle from attending-level spending back toward resident-style living.

That one mindset shift changed everything.

What they actually did to pay off $100,000 so fast

1. They made a real budget, not a polite suggestion

Once the household moved into a lower-cost setup, they wrote down what they truly needed. That sounds simple, but it is the step most high earners avoid because it is annoyingly effective. Budgets are not fun. They are mirrors. And mirrors have no interest in your excuses.

This physician’s family cut recurring expenses across the board. Grocery shopping shifted from premium stores to discount stores. Cable was cut. Cell phone costs were reduced. Work lunches were replaced with batch cooking. Vehicle maintenance was handled more cheaply. Even haircuts got the DIY treatment. None of those moves are sexy. Together, they were powerful.

2. They refinanced the student loans

After refinancing, the student loan balance sat around $208,000 at 3.875%. That math changed the emotional game. At the old pace, the debt felt like a swamp. At the new rate, it became a target. The family realized that paying $7,000 a month could wipe out the loans far sooner than expected and significantly reduce interest costs over time.

This is where physician debt payoff gets practical instead of dramatic. Once borrowers can see the monthly payment needed for a two-year or three-year payoff, the fog starts to clear. A debt that felt immortal suddenly has a calendar.

3. They used both monthly cash flow and lump sums

In six months, the family sent about $44,000 from regular monthly budgeting and another $36,000 from bonuses and tax refunds toward the loans. Then they looked at their emergency fund and made a bold decision: keep $10,000 and direct the rest toward debt. That final push produced the headline number, bringing total loan repayment to $100,000 in six months.

This matters because rapid debt payoff is rarely a story about one gigantic heroic payment. More often, it is a stack of smaller decisions: lower bills, redirected bonuses, fewer upgrades, leaner housing, and purposeful use of windfalls. The lump sums finish what the monthly budget starts.

4. They found visible motivation

The physician even created a physical reminder to track progress. That may sound silly until you remember that debt is emotional. Logic gets you started, but momentum keeps you going. This is why so many people swear by debt charts, loan thermometers, payoff apps, and calendar countdowns. Numbers become easier to attack when they stop being abstract.

Why this strategy worked so well

At first glance, the story sounds like a master class in frugality. It is. But the deeper reason it worked is that the family attacked the problem from three angles at once: fixed costs, interest rate, and payment size.

Many borrowers only focus on one lever. They either trim expenses but ignore loan structure, or refinance but keep spending high, or talk about paying off debt quickly without ever deciding what “quickly” means in dollars. This family used all three levers. They lowered ongoing expenses, improved the loan terms, and committed real cash every month.

That is the difference between “being concerned about debt” and “running a debt payoff campaign.” Concern is a feeling. A campaign has numbers.

Could another physician do this today?

Yes, but with an important asterisk: today’s physician has to choose the right lane first. Medical education debt is still a major issue. A large share of medical students graduate with debt, and many balances are deep into six figures. At the same time, physician income remains strong overall, even if inflation, geography, taxes, and practice setting can shrink the real-world impact of a big salary. Translation: doctors can absolutely crush debt, but not every doctor should use the exact same playbook.

For example, a physician pursuing Public Service Loan Forgiveness or another federal forgiveness track should be very cautious about refinancing federal student loans into private loans. Lower interest can look attractive, but it may come at the cost of valuable federal protections and forgiveness eligibility. On the other hand, a physician in private practice or a higher-income attending role with no forgiveness plan may find refinancing to be one of the most effective moves available.

That is why the first question is not, “How fast can I pay this off?” The first question is, “Am I pursuing forgiveness or aggressive payoff?” Get that wrong, and everything else gets wobbly.

The debt payoff blueprint physicians can borrow from this story

Pick your lane: forgiveness or speed

Before sending extra money anywhere, decide whether you are a forgiveness borrower or an aggressive payoff borrower. If your job, loan type, and long-term plans make forgiveness realistic, your best move may be to minimize required payments and maximize qualifying months. If not, speed matters. This physician’s success came from fully committing to speed instead of half-saving, half-spending, and half-paying debt forever. Financially speaking, “sort of” is expensive.

Audit every loan and every interest rate

List the balance, interest rate, minimum payment, servicer, and loan type for everything. Student loans, car loans, personal loans, and credit cards should all go on the page. If you are going to attack debt seriously, you need the map before the marching orders. This is also the moment to check your credit reports for errors, because mistakes can affect the rate you qualify for if you refinance.

Choose a repayment method you will actually stick with

Some borrowers love the debt avalanche method, which prioritizes the highest-interest debt first and usually saves the most money. Others prefer the debt snowball, which knocks out smaller balances first and creates quick wins. Mathematically, avalanche often wins. Psychologically, snowball often feels better. The best method is the one that keeps you paying next month, not the one that merely impresses a spreadsheet.

In this physician’s case, the payoff had snowball energy because momentum mattered, but it also had avalanche discipline because high-cost debt was not being politely left alone to reproduce in the corner.

Keep a lean emergency fund, not a fantasy fortress

Aggressive debt payoff does not mean being reckless. It means being strategic. A modest emergency fund can protect against car repairs, travel emergencies, or surprise bills while still allowing excess cash to hit high-interest debt. This physician did not reduce savings to zero. She reduced them to a practical number and then treated the debt itself as the emergency. That is a very different mindset from draining every dollar into a vague “just in case” pile while expensive interest keeps chewing through your future.

Attack fixed costs first

Variable spending matters, but fixed costs are the heavyweights. Housing, car payments, insurance, childcare, and subscriptions shape your monthly life far more than the occasional latte ever will. This family’s move from attending-style housing to a more modest rental created breathing room that small spending cuts alone could never match.

If a physician wants a six-figure debt payoff sprint, the easiest question is usually not, “Should I stop ordering takeout?” It is, “Why am I spending like I own a yacht when I still owe Sallie Mae enough money to buy one?”

Direct every windfall with intention

Bonuses, tax refunds, signing bonuses, relocation packages, moonlighting income, extra shifts, locum tenens pay, and side consulting checks can become debt napalm if they are assigned before they arrive. If you wait until the money lands in your checking account, the brain immediately starts composing a very moving speech about how you deserve a kitchen renovation.

Do the opposite. Decide in advance. Write it down. Make the transfer quickly. Let the money have a mission before it develops hobbies.

How physicians can create extra payoff power

Not every doctor can cut their way to a dramatic debt payoff. Sometimes the real move is increasing income. This is especially relevant for attendings, late-stage residents, fellows, or physicians in flexible practice models.

Moonlighting is one obvious option. Residents and physicians have long used additional shifts to create faster loan progress, though the tradeoff is fatigue, scheduling strain, and possible burnout. Side income can also come from consulting, teaching, chart review, telemedicine, locum tenens work, or other clinical and nonclinical roles. Even a temporary income boost can compress a payoff timeline dramatically when the money goes straight to principal instead of lifestyle inflation.

Signing bonuses can play a similar role. For a new attending, a bonus is not just a welcome gift. It can be a financial accelerant. Used well, it can erase a chunk of principal before interest gets too comfortable. Used poorly, it becomes patio furniture with a tax bill.

The mistakes that keep physicians in debt longer than necessary

Confusing high income with high margin

Doctors often earn strong incomes, but strong income is not the same as free cash flow. Taxes, retirement contributions, family costs, and expensive fixed obligations can eat enormous portions of gross pay. If you do not know your monthly surplus, you do not yet know your debt strategy.

Buying the “I’m finally an attending” package

House upgrade. Luxury SUV. Furniture that looks like it was selected by a home-design influencer named Aspen. None of these are evil. They are just very committed to making your debt stick around longer. The physician in this story made progress when the household stopped rewarding every career milestone with another payment.

Refinancing without understanding what you give up

Refinancing can be powerful, but it is not universally wise. Federal loans carry certain protections and forgiveness possibilities that private loans do not. Lower rates are great. Accidentally disqualifying yourself from a valuable federal path is not.

Saving in a way that secretly helps debt survive

Yes, savings matter. But there is a difference between healthy liquidity and strategic avoidance. Parking large sums in low-yield cash while carrying costly debt can be a very expensive form of emotional support.

What this payoff story really teaches

The biggest lesson is not “live on rice and beans” or “never have fun again.” The biggest lesson is that alignment beats income. When spending, loan structure, and priorities all point in the same direction, big progress can happen shockingly fast.

This physician did not become happier because debt disappeared overnight. She became happier because the household finally stopped sending mixed signals. Their calendar, housing, spending, and financial goals started telling the same story. They traded status for breathing room. They traded image for momentum. They traded “we should really deal with this someday” for “we are dealing with it now.”

That is why the six-month payoff matters. It was not just about cutting a balance. It was about restoring control.

Additional physician experiences that prove this is not a one-off miracle

If this story sounds extraordinary, that is because most people only hear the dramatic number at the end and not the long trail of choices behind it. But versions of this same pattern show up again and again in physician finance. Different specialties, different cities, different debt totals, same core principle: once doctors stop inflating their lifestyle and start assigning every extra dollar a mission, debt starts moving.

Consider the physician who graduated residency carrying about $315,000 in medical school debt and chose a more aggressive payoff strategy through locum tenens work rather than stretching repayment over a decade. The exact circumstances were different, but the logic was familiar: increase cash flow, control overhead, and shorten the timeline on purpose. That approach is not for everyone, especially if schedule flexibility or geographic mobility is limited, but it shows how income design can matter just as much as budgeting.

Or look at the family medicine couple who left training with roughly $450,000 in debt. Loan repayment programs covered a big portion, but the remaining balance did not vanish by motivational poster. They still had to moonlight, live frugally, and continue making disciplined decisions. That matters because it corrects a common myth. Outside help is great, but even generous repayment support usually works best when paired with boring, repeatable habits.

Then there is moonlighting, which keeps appearing in physician debt stories for one very simple reason: extra shifts create concentrated cash. A physician who sends an extra few thousand dollars a month to debt does not just lower a balance. They reduce future interest, shrink the psychological weight of the loan, and often reclaim flexibility faster than they expected. The caution, of course, is burnout. Extra income is only helpful if it does not wreck your health, your training, or your family life in the process.

New attendings also have another lever that older advice sometimes overlooks: the job offer itself. A signing bonus, relocation package, or other up-front incentive can provide an unusually clean opportunity to slam principal before lifestyle inflation has time to unpack its boxes. The mistake is treating these funds like celebration money. The smarter move is to let the celebration be a lower balance and fewer years of obligation.

What ties all these experiences together is not deprivation. It is intentionality. The physicians who make dramatic progress are rarely the ones with the prettiest spreadsheets. They are the ones who decide, clearly and a little stubbornly, that debt is not getting the best decade of their career. Sometimes that means refinancing. Sometimes it means moonlighting. Sometimes it means renting longer, delaying the luxury car, or living like a resident for just a bit more time. None of that is glamorous. But neither is dragging six figures of debt behind you like a parade float you never wanted.

Conclusion

So, how did this physician pay off $100,000 in debt in 6 months? Not through wizardry. Through clarity. She cut fixed costs, refinanced strategically, budgeted aggressively, redirected windfalls, kept a practical emergency reserve, and stopped spending like the debt was somebody else’s problem. That combination turned a crushing balance into a shrinking one.

For physicians staring down medical school loans, the takeaway is surprisingly hopeful. You do not need a perfect personality, a flawless budget, or an ascetic existence. You need a lane, a plan, and enough consistency to keep your income from evaporating into the nice-but-not-necessary parts of modern doctor life. Debt payoff is rarely one giant heroic act. It is usually a hundred unglamorous decisions that finally start pulling in the same direction.

And that, more than the headline, is the real win.