Table of Contents >> Show >> Hide

Let’s clear something up before the internet faints onto a chaise lounge: the best loopholes are not shady, illegal, or likely to get you a dramatic phone call from “the authorities.” The clever loopholes people actually don’t regret exploiting are the boringly beautiful ones hidden in policies, perks, tax rules, return windows, and loyalty programs. In other words, they’re the benefits you get when you stop assuming the rules are working against you and start reading the fine print like it owes you money.

And sometimes, it really does.

That is why so many people say the same thing after a few years of getting smarter with their spending: “I can’t believe I used to pay full price for that.” Whether it is stacking rewards, claiming tax breaks, using free government tools, or timing purchases with the patience of a cat staring at a bird feeder, these everyday loopholes are less about cheating the system and more about finally understanding it.

What Counts as a “Clever Loophole” Here?

For this article, a clever loophole means a legal, ethical, real-world strategy that works because most people either do not know it exists or do not bother to use it. These are the kinds of loopholes that save money, reduce stress, and make you feel mildly invincible in the checkout line.

47 Clever Loopholes People Keep Using Because They Actually Work

Shopping and Retail Loopholes

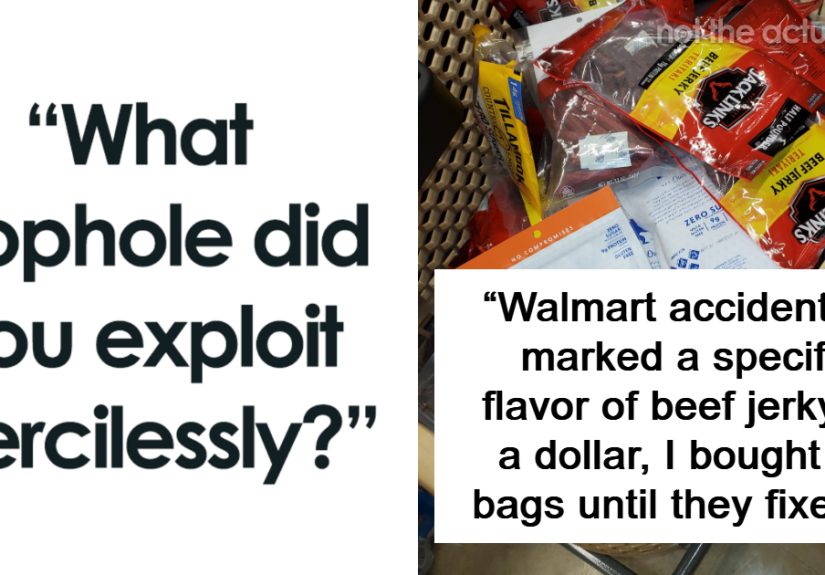

- Ask for a price adjustment after you buy. Plenty of stores will refund the difference if the price drops shortly after your purchase. The loophole is simple: most shoppers never ask.

- Use price matching before checkout. A lot of retailers would rather keep your business than lose it over a lower posted price somewhere else. One screenshot can suddenly turn you into the smartest person in aisle seven.

- Stack the deal, don’t just take the deal. Sale price, store coupon, credit card offer, shopping portal, and cash-back app can sometimes work together. One discount is nice. Five discounts is performance art.

- Click through a shopping portal first. Rewards portals and card-linked offers can pile extra points or cash back on top of what you were already going to earn. The key is not shopping first and remembering the portal later, which is the budgeting version of crying over spilled milk.

- Buy open-box when the return policy is still intact. Open-box electronics, appliances, and tools often come with a lower price but far less real-world risk than people imagine. Sometimes the “defect” is simply that someone else panicked and returned it.

- Choose refurbished from the manufacturer or an authorized seller. Refurbished does not automatically mean sketchy. In many cases, it means inspected, tested, discounted, and much easier on your wallet.

- Negotiate on big-ticket purchases. Mattresses, appliances, furniture, and floor models are still haggling territory more often than people realize. The loophole is remembering that the sticker price is not a sacred text.

- Use first-order discounts strategically. If a store offers a legitimate sign-up coupon for joining email or text alerts, take it on the purchase you were already planning to make. Then unsubscribe before your inbox becomes a clearance bin with feelings.

- Wait for predictable sales cycles. A “limited-time offer” is sometimes just a store’s monthly personality. If you know the category, you can often wait out the fake urgency and buy when the real markdown lands.

- Watch for extended holiday return windows. A regular return policy may become dramatically more generous during gift-buying season. That extra time can save you from buyer’s remorse and from pretending you absolutely love the blender in March.

- Use cart abandonment to your advantage. Leaving an item in your cart does not always unlock a discount, but it occasionally triggers a reminder or promo code. No guarantee, but the internet rewards mild emotional distance.

- Remember the cooling-off rule for certain away-from-store sales. Some purchases made at your home, workplace, dorm, or temporary sales location may come with a cancellation window. That is not a scammer’s loophole. That is your loophole.

Travel, Delivery, and Everyday Mobility Loopholes

- Join loyalty programs even if you are not a frequent traveler. Free membership can unlock lower member pricing, easier tracking, and occasional perks. You do not need to become a suitcase influencer to benefit.

- Use airline and hotel shopping or dining programs. People obsess over flights and forget the quiet little loophole of earning rewards while buying normal things. Coffee, shoes, and dinner can all secretly cosplay as travel strategy.

- Travel on the least glamorous days. Off-peak flights, midweek stays, and weirdly timed departures are often cheaper because they are less convenient. Turns out inconvenience is occasionally a coupon code written by fate.

- Pack carry-on only when the math works. For short trips, skipping checked baggage can slash the true cost of a “cheap” fare. The loophole is not overpacking like you are fleeing civilization forever.

- Choose hotels that bundle value instead of chasing the lowest nightly rate. Free breakfast, parking, transit access, and late checkout can beat a lower base price with a dozen annoying add-ons.

- Use USPS Hold Mail when you travel. It is a free way to avoid a stuffed mailbox advertising your absence to the world. Not flashy, but neither is identity theft.

- Sign up for USPS Informed Delivery. Getting previews of incoming mail is a weirdly satisfying administrative superpower. It helps you catch important documents, missed bills, and the suspicious absence of something that should have arrived.

- Use the Every Kid Outdoors pass if your family qualifies. Families with an eligible fourth grader can unlock free access to federal lands and waters. Sometimes the best travel loophole is a kid who still thinks rocks are treasure.

Money, Banking, and Credit Card Loopholes

- Use the credit card grace period correctly. When you pay the statement balance on time, you can borrow for a short period without interest. Used well, this is cash-flow management. Used badly, it is a lecture from your future self.

- Set autopay as a safety net, not a substitute for attention. Many smart users set autopay for the minimum payment so they never get hit with a late fee, then manually pay the full statement balance before interest becomes a problem.

- Stop unwanted preauthorized debits before they hit. People often assume recurring payments are unstoppable once authorized. They are not. Learning your stop-payment rights is one of the least glamorous and most satisfying loopholes in modern life.

- Opt out of debit card overdraft coverage if fees are the real product. Many people do not realize banks generally need your opt-in for certain debit and ATM overdraft fees. Not choosing the fee trap is a deeply underrated financial hobby.

- Use an HSA as more than a medical piggy bank. A health savings account can offer powerful tax advantages for eligible users. Some people pay current medical bills out of pocket and leave the HSA invested for later, which is the kind of sentence that makes personal finance nerds tear up.

- Check whether your FSA includes a carryover or grace period. Too many people race to buy panic bandages in December because they assume unused funds vanish instantly. Your plan may be kinder than your office rumor mill.

- Claim the Saver’s Credit if you qualify. Retirement contributions can sometimes earn a tax credit on top of the long-term savings benefit. Yes, the government occasionally rewards responsible behavior. Rare, but touching.

- Use 529 plans for tax-advantaged education saving. Families often focus on tuition panic later instead of tax-smart planning earlier. The loophole is making education money work before it is needed.

- Do not ignore education tax benefits. Credits, tuition-related breaks, and other education benefits are commonly missed simply because people assume filing software will do all the thinking for them. That is a brave assumption.

- Claim the Child and Dependent Care Credit if you are eligible. If you are paying for care so you can work or look for work, that expense may help reduce your tax burden. Childcare is expensive enough without leaving legal relief on the table.

- Use employer dependent care benefits when available. Some workplaces quietly offer tax-advantaged dependent care help that employees forget exists. Human Resources may not be thrilling, but sometimes it is secretly profitable.

- Check your card’s built-in protections before buying extras. Rental coverage, purchase protection, extended warranties, and trip benefits can already be sitting on your card. Buying duplicate coverage is the financial equivalent of paying twice for the same sandwich.

- Use cash back or rewards for categories you already spend on. The loophole is not earning points. The loophole is refusing to change your whole personality just because a card offers 5% back on camping lanterns.

Health, Medicine, and Insurance Loopholes

- Ask whether a generic works. Generic medicine often delivers the same active ingredient at a lower price. Paying extra for the brand name is sometimes just paying for prettier marketing.

- Compare 30-day fills with 90-day or mail-order options. For maintenance medications, the longer fill can be significantly cheaper and more convenient. Fewer pharmacy trips, fewer chances to forget, fewer moments of “Why is this suddenly $42 more?”

- Review every hospital or medical bill like it insulted your family. Duplicate charges, wrong quantities, and billing errors are not myths. Quietly accepting them is not a personality trait to keep.

- Ask about cash-pay discounts and no-interest payment plans. Medical billing departments are not always eager to advertise flexible options, but that does not mean they do not exist. The awkward phone call can be worth hundreds.

- Apply for Medicare Extra Help if you may qualify. Prescription assistance is one of those programs many people need and too many people never pursue. Complexity is not the same thing as disqualification.

- Use urgent care when it is appropriate instead of reflexively choosing the ER. This is not a loophole for emergencies, of course. It is a loophole for all the not-quite-emergency moments that can still punish your wallet.

Home, Family, Work, and Lifestyle Loopholes

- Split qualifying home energy upgrades across tax years when annual caps apply. Timing matters. A project spread out thoughtfully can unlock more value than doing everything in one expensive burst.

- Stack federal incentives with local utility or state programs when allowed. People often stop at one rebate and miss the second or third layer. Bureaucracy is annoying, but occasionally it comes bearing coupons.

- Use student, educator, military, senior, or professional discounts when you actually qualify. Too many people age into savings, job into savings, or credential into savings and never cash in.

- Check alumni benefits before assuming graduation ended the perks. Discounts, software access, job boards, and continuing resources sometimes linger longer than school spirit. The cap and gown may be gone, but the discount code survives.

- Borrow before buying through your local library. Books are the obvious part. The less obvious part is ebooks, audiobooks, classes, streaming access, and in some communities, even passes and tools. Public libraries remain one of America’s most underused flexes.

- Audit your phone, internet, and subscription bundles. Free streaming trials, bundle credits, loyalty offers, and grandfathered rates hide in plain sight. The loophole is reading the bill before it reads you.

- Use employee purchase programs and commuter benefits. Workplace perks are often treated like corporate wallpaper: technically visible, functionally ignored. Some of them are worth real money.

- Buy discounted gift cards for planned purchases, not emotional chaos. This works only when you already know where you will spend the money. Otherwise you are not hacking the system. You are buying yourself future confusion.

- Downgrade subscriptions instead of canceling into nothing. A lower tier, annual plan, or ad-supported version can keep the value while cutting the cost. Not every relationship needs to end dramatically.

- Ask for a retention offer before you leave. Cable, internet, software, gyms, and subscription services often discover surprising affection for you once cancellation appears on the horizon. Miracles happen every day.

Why These Loopholes Work So Well

Most of these tactics work for one simple reason: companies, systems, and even government programs quietly rely on user inattention. They count on people forgetting to ask, missing a deadline, assuming they are not eligible, or being too tired to compare options after a long day. That is why the best loopholes rarely feel dramatic. They feel administrative. The savings come from noticing.

That is also why these loopholes age so well over time. One coupon is nice. One tax break is useful. But the real magic is repetition. When a person gets into the habit of checking return policies, reviewing benefits, claiming credits, and stacking value carefully, the savings stop being random. They become structural.

What Four Years of Using These Loopholes Actually Feels Like

People who have been using these methods for years usually do not describe the experience as thrilling. They describe it as quietly life-improving. At first, the habit feels small: asking customer service for a price adjustment, signing up for a free mail alert, finally opening the benefits guide at work instead of using it as a coaster. Then a few months pass, and the pattern starts to reveal itself. Groceries cost less. Travel feels less chaotic. Tax season goes from mild dread to “Wait, we qualified for that?”

One parent might start with something simple, like using a child-related tax break they had ignored before, then realize the family also qualifies for a free pass to outdoor sites, then notice the pharmacy can fill a maintenance prescription at a lower 90-day price. None of those wins sounds huge in isolation. Together, they create breathing room. And breathing room is one of the most underrated luxuries in American life.

A renter might learn to stack online shopping rewards with a sale and a card offer, then carry that same mindset into utilities, subscriptions, and work benefits. A traveler might begin by joining a loyalty program for one trip and end up using dining rewards, free mail tools, and better hotel math for every trip after that. A homeowner might stop assuming every upgrade is just an expense and start thinking in terms of timing, credits, rebates, and total household efficiency. Suddenly, “expensive” and “worth it” are not enemies anymore.

The emotional shift is just as important as the financial one. After a few years, people stop feeling like money only moves in one direction. They stop treating prices as fixed, policies as mysterious, and bills as uneditable. They become more willing to pause, compare, call, ask, and verify. In a culture built on hurry, that tiny refusal to rush is its own loophole.

And no, this does not turn ordinary people into spreadsheet goblins who whisper sweet nothings to cashback apps under the moonlight. It usually just makes them calmer. The person who knows how to stop a bad auto-debit, check a bill, or claim a tax benefit is not gaming the world. They are finally participating in it with their eyes open.

That may be the real lesson behind the whole “I’ve been using this method for over four years” mindset. The method is not one trick. It is a way of thinking. It is the habit of asking, “What does the fine print actually allow me to do?” That question, asked often enough, becomes a financial personality upgrade. Not flashy. Not criminal. Just smart, repeatable, and oddly satisfying.

Final Takeaway

The loopholes people never regret exploiting are almost never the wild ones. They are the ethical, boring, money-saving advantages hiding in everyday systems: return rules, banking rights, tax credits, medical savings, travel perks, and discounts that most people simply never claim. Once you start spotting them, you realize the world is full of “small print” that can work in your favor. And that, frankly, is a much better plot twist than paying full price forever.