Table of Contents >> Show >> Hide

- What “Dunking on Doomers” Really Means (And What It Doesn’t)

- Why Animal Spirits Hits a Nerve

- Animal Spirits: The Original Meaning (And Why It Matters Now)

- The Psychology of Doomerism (Aka: Why Bad News Feels Like “The Truth”)

- Common Sense Data Points That (Gently) Humble Doomers

- So What Do You Do Instead? A Dunking-on-Doomers Toolkit

- How the “Dunking on Doomers” Episode Frames the Real World

- When Doomers Are Actually Useful

- Conclusion: A Wealth of Common Sense Is a Competitive Advantage

- Real-World Experiences: What “Dunking on Doomers” Looks Like in Practice (Extra)

There are two types of people in investing: the ones who believe the market is a complicated discounting machine…

and the ones who believe it’s a haunted house where every creak is a recession hiding in the closet.

“Dunking on doomers” sits right at the intersection of those worlds. It’s the moment someone predicts financial

Armageddon for the eighth time this quarter, and you respond with the deadliest weapon in personal finance:

calm, boring, evidence-based common sense.

That’s also the vibe behind Animal Spiritsthe markets-and-life podcast hosted by Michael Batnick and Ben Carlson,

the creator of A Wealth of Common Sense. Their style isn’t “ignore risks” or “everything is fine.”

It’s more like: “Yes, uncertainty is real. Also, panic is optional.”

What “Dunking on Doomers” Really Means (And What It Doesn’t)

In investing slang, a “doomer” is someone who’s always convinced the next crash is imminentand often acts like

the only responsible move is to sit in cash until the world feels safe again. The “dunk” isn’t about mocking people

for being cautious. It’s about pushing back on the false idea that fear equals wisdom.

Here’s the important nuance: doomers aren’t always wrong about the existence of problems. Markets can fall, recessions

happen, bubbles pop, and headlines can reflect real pain. The issue is the conclusion doomers tend to jump to:

because the world is messy, the only rational move is to stop investingor to constantly trade based on scary narratives.

“Dunking” is shorthand for a better conclusion: if you have goals that span years (or decades), your strategy should be

built to survive uncertainty, not require certainty. That’s not bravado. That’s portfolio design.

Why Animal Spirits Hits a Nerve

Part of what makes Animal Spirits different is that it doesn’t treat investing like a spreadsheet-only lifestyle.

The show jumps between market structure, investor psychology, economic data, and pop culturebecause that’s how real

people actually experience money. You don’t invest in a vacuum. You invest while reading news, feeling stress, watching

your feed, and trying to live your life.

Ben Carlson’s writing on A Wealth of Common Sense is cut from the same cloth: markets are complicated,

but your behavior doesn’t have to be. You can build a solid plan, stick to it, and avoid self-sabotage.

That’s the “wealth of common sense” promise in a sentence.

Animal Spirits: The Original Meaning (And Why It Matters Now)

“Animal spirits” is an old-school phrase with modern relevance. Economist John Maynard Keynes used it to describe how

human emotionsconfidence, fear, optimism, pessimismshape economic decisions when the future is unknowable.

Translation: people aren’t robots, and markets aren’t purely mechanical.

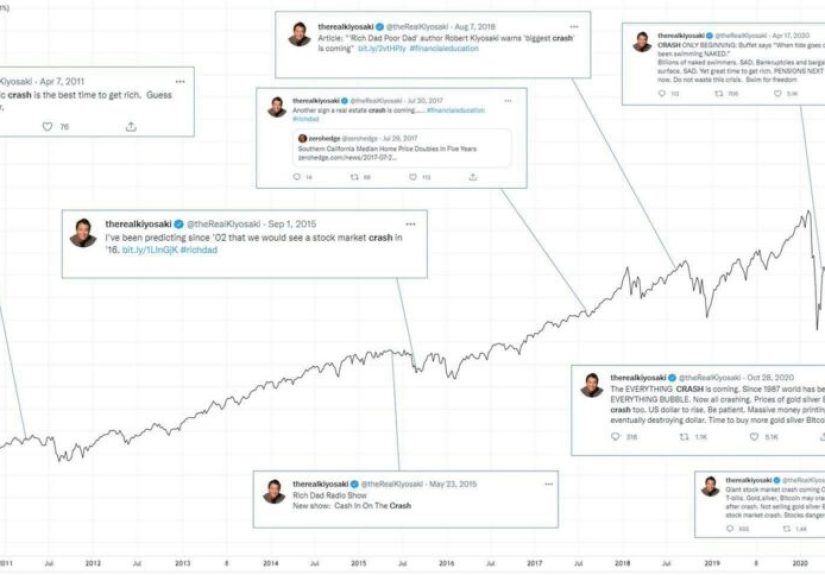

That’s exactly why doomer narratives spread so fast. Doom is emotionally sticky. It offers a clean story:

“Everything is broken, therefore the only smart move is to do something dramatic.”

And dramatic feels productiveeven when it’s expensive.

The Psychology of Doomerism (Aka: Why Bad News Feels Like “The Truth”)

1) Negativity bias is a feature, not a bug

Humans evolved to notice threats. That’s useful when the threat is a bear. It’s less useful when the threat is a

headline designed to maximize clicks. Your brain treats bad news like a smoke alarm: loud, urgent, and hard to ignore.

2) Availability is not probability

If you’ve recently lived through a market drawdown, your mind can start treating that pain as the “default setting.”

Suddenly, every dip looks like 2008, every inflation print looks like the 1970s, and every tech rally looks like 1999.

Sometimes those comparisons are insightful. Often, they’re just mental shortcuts pretending to be forecasts.

3) Stories beat statistics

A doomer story is usually simple, vivid, and repeatable: “The system is rigged,” “A crash is inevitable,” “This time is different.”

Meanwhile, reality tends to be messy: economic data is mixed, markets price expectations, and outcomes arrive in weird combinations

(like “inflation falls but anxiety stays high”).

Common Sense Data Points That (Gently) Humble Doomers

A “dunk” lands best when it’s not a hot takeit’s a reminder of how markets and people actually behave.

Here are a few evidence-backed ideas that show up again and again in smart investing conversations.

Markets often recover before you emotionally feel safe

This is one of the cruelest truths in investing: the market tends to rise during periods when the news still feels grim.

That’s not because markets are heartless. It’s because markets are forward-looking. Prices move on expectations,

not on your personal comfort level.

The practical takeaway isn’t “ignore reality.” It’s “don’t require a perfect emotional environment to follow your plan.”

If your strategy depends on you calling the exact bottomor waiting until the coast is visibly clearit’s not a strategy.

It’s a wish with a brokerage account.

Missing the best days can do long-term damage

Market timers love the fantasy of sidestepping every sell-off. The problem: the best days often cluster around the worst days.

If you’re out of the market “until things settle down,” you can miss the rebound that does most of the heavy lifting.

Studies illustrating this point aren’t subtle. Over long stretches, missing a handful of top-performing days can significantly

reduce annualized returns. The numbers vary by period and methodology, but the message is consistent:

being invested matters more than being clever.

The “behavior gap” is real: investors often earn less than the funds they own

Here’s a doomer plot twist: sometimes the biggest risk isn’t the marketit’s the investor.

Research on “investor returns” versus “total returns” shows that timing decisions (adding money after a run-up,

pulling money after a drop) can reduce what people actually earn compared with what a fund earned over the same period.

In plain English: you can buy a good investment and still get bad results if you treat it like a hot potato.

The doomer mindset can amplify this. If you’re constantly bracing for disaster, you may sell at the exact moment

you’re locking in lossesand then hesitate to reinvest until prices are higher and optimism is fashionable again.

Active outperformance is harder than it looks (especially after fees)

Doom narratives sometimes push people toward frantic “tactical” moves: rotating sectors, chasing the “next safe thing,”

or paying up for anyone who claims they can dodge the next downturn. The trouble is that consistent outperformance is rare,

and the odds often worsen over longer time horizons.

None of this means active investing is “bad.” It means the burden of proof is highand the doomer urge to constantly

do something can turn investing into an expensive hobby.

So What Do You Do Instead? A Dunking-on-Doomers Toolkit

If doom is a vibe, common sense is a system. Here are practical ways to protect yourself from fear-based decision-making

without pretending risks don’t exist.

1) Turn scary headlines into a checklist

- Time horizon: Do I need this money in 12 months, or 12 years?

- Cash needs: Do I have an emergency fund so I’m not forced to sell at a bad time?

- Allocation: Is my stock/bond mix appropriate for my risk toleranceor am I overexposed?

- Diversification: Am I betting my future on one sector, one theme, or one “sure thing”?

- Plan: If markets drop 20%, do I already know what I’ll do?

Doom thrives in ambiguity. A checklist reduces ambiguity.

2) Automate your “good behavior”

One reason dollar-cost averaging and consistent contributions (like retirement plan deposits) can work so well is that

they remove the need to time the market. You invest in up markets, down markets, weird markets, and “everyone on the internet

is yelling” markets. The routine becomes the strategy.

3) Rebalance like a grown-up

Rebalancing is a polite way of doing the opposite of what your emotions want. When stocks run up, you trim a little.

When stocks fall, you top up a little (assuming your plan calls for it). It’s not flashy. It’s not viral.

It’s also one of the simplest disciplines that can keep your risk level aligned with reality.

4) Treat forecasts like weather apps: useful, not sacred

Forecasts can help you think in ranges and scenarios. They’re great for planning.

They’re terrible as a trigger for all-in, all-out portfolio decisions.

The doomer move is to treat a forecast like a prophecy. The common-sense move is to treat it like a reminder that

uncertainty existsand that your plan should be resilient anyway.

5) Upgrade your “information diet”

If your media consumption leaves you panicked, angry, or convinced collapse is imminent, you don’t have an “information diet.”

You have an emotional sabotage pipeline.

Consider a simple rule: get market news on a schedule (weekly, for example), and focus daily attention on what you can control

(saving rate, spending, skills, health, relationships). Doom hates this rule because it works.

How the “Dunking on Doomers” Episode Frames the Real World

The fun of an Animal Spirits episode like “Dunking on Doomers” is that it’s not a lecture. It’s a tour of the

cultural and financial momentmixing charts, headlines, and internet reactions. The underlying theme is consistent:

the world is complicated, but that doesn’t automatically justify extreme investing behavior.

In that particular moment, the conversation touched on topics like shifting fund flows, labor market vibes,

inflation narratives, housing myths, and the way public mood can lag behind improving data. That’s an important point:

sentiment and fundamentals don’t move in lockstep.

Doom sometimes shows up when the data is improving (because people are still feeling yesterday’s pain).

Optimism sometimes shows up when risks are building (because people are still celebrating yesterday’s wins).

The job of an investor isn’t to perfectly match the mood. It’s to keep a plan steady across mood swings.

When Doomers Are Actually Useful

Let’s be fair: doomers can provide value when they force you to stress-test assumptions.

“What could go wrong?” is a healthy question. The problem is when it becomes the only question.

A productive way to use doomer energy:

- Run scenarios: “If markets fall 30%, what changesif anythingin my spending or timeline?”

- Build buffers: emergency fund, insurance coverage, reasonable debt levels.

- Avoid fragility: reduce reliance on one employer, one asset, or one risky bet.

Notice what’s missing: “Sell everything because someone on social media used the word ‘collapse.’”

Conclusion: A Wealth of Common Sense Is a Competitive Advantage

“Animal spirits” aren’t going away. Markets will always be fueled partly by emotion, narrative, and confidence.

And doom will always be available in high definition.

The point of “dunking on doomers” isn’t to deny risk. It’s to refuse fear-based shortcuts.

Build a plan that assumes volatility, diversify so you don’t need a single prediction to be right,

invest consistently, and let time do what time does best: compound.

The real flex in investing isn’t winning arguments on the internet. It’s reaching your goals while other people

spend decades chasing certainty that never arrives.

Real-World Experiences: What “Dunking on Doomers” Looks Like in Practice (Extra)

Experience #1: The “I’ll reinvest when it feels safe” loop.

A classic pattern goes like this: someone sells after a sharp drop because they’re “being responsible,” then waits for a sign

that the market is stable. But stability is usually visible only after prices have already moved higher. Months later, they face

an awkward choice: buy back in at higher prices (and admit the sell was costly), or keep waiting (and keep drifting from the plan).

The most painful part is that the original impulse was understandablenobody likes watching account balances fall. The fix is also

simple, but not easy: decide in advance what triggers a change (if anything), and treat “fear” as a feeling, not an instruction.

Experience #2: The doom headline that doesn’t match daily life.

Many investors describe a weird disconnect: their feeds suggest everything is falling apart, but their actual lives look… normal.

Work is busy, people are still traveling, restaurants are still full, and the world feels more “messy” than “ending.”

That disconnect can create decision paralysisbecause if you believe the doom story, you feel you should sell, but if you believe

your lived reality, selling feels extreme. A common-sense approach bridges the gap: acknowledge real problems, then ask whether your

portfolio is built for resilience (diversification, an emergency fund, and a time horizon long enough to absorb volatility).

Experience #3: The “all-cash = peace” illusion.

Going to cash can feel soothing because it reduces daily market drama. But that calm can be deceptive. Cash still has risks:

inflation risk, opportunity cost, and the risk that you never find a “perfect” time to re-enter. Investors often report that once they

move to cash, the emotional bar for reinvesting risesbecause now they feel responsible for choosing the exact right moment.

The solution that shows up in a lot of steady investing stories is a compromise: keep a planned cash cushion for near-term needs,

and invest the long-term portion according to a written allocation. Peace comes less from predicting markets and more from separating

“money I need soon” from “money I’m growing over time.”

Experience #4: The “news detox” experiment that changes behavior.

Investors who step back from constant market news often describe the same surprise: they don’t become uninformedthey become less reactive.

A weekly check-in replaces hourly refreshes. A monthly contribution replaces impulsive trades. Instead of “What did the market do today?”

the question becomes “Am I still on track?” That shift is basically dunking on doomers in real life: not by arguing with scary narratives,

but by refusing to let them hijack your process. When you reduce noise, your plan gets louder. And a loud plan is a doomer’s natural predator.